How Do You Start an Investment Company? A Step-by-Step Guide

Wondering how do you start an investment company? Learn key steps for legal setup, fundraising, and launching your own successful investment firm.

So, you’re thinking about launching an investment firm. It's an ambitious goal, involving everything from navigating a maze of legal requirements to raising capital and building an entire operational infrastructure from scratch. But before any of that, it all starts with one powerful, defensible idea. That's what will set you apart.

Defining Your Edge in a Crowded Market

Before you even think about drafting legal docs or pitching investors, you have to answer the most important question: why should anyone give you their money? The answer is the bedrock of your entire firm. Without a killer edge, even a perfectly structured company will fail to attract capital. This is where you dig your strategic moat.

Answering this question isn't about crafting a fuzzy mission statement. It’s about forging a razor-sharp investment thesis—the core philosophy that will drive every single decision you make. This thesis is your filter, telling you which deals to chase and, more importantly, which to walk away from. It's the story you'll sell to partners, LPs, and your future team.

Crafting a Unique Investment Thesis

Your thesis needs to be specific enough to have teeth but flexible enough to ensure you actually have deals to look at. A goal like "investing in good tech companies" isn't a thesis; it's a wish. A truly effective thesis marries a specific market focus with a unique operational playbook.

Think about it in concrete terms. Here are a few real-world angles:

- Sector and Stage Focus: A thesis centered on "pre-seed B2B SaaS companies in the American Midwest" is incredibly specific. It immediately carves out a niche by targeting a geography many coastal VCs ignore.

- Strategy-Driven Focus: You could build a fund around "distressed commercial real estate in Sun Belt secondary markets." This approach is designed to capitalize on demographic trends and economic cycles to find undervalued assets.

- Impact-Oriented Focus: Your thesis might be "growth-stage companies developing sustainable packaging solutions," which resonates strongly with a growing class of environmentally conscious Limited Partners (LPs).

Your investment thesis is your firm's North Star. It’s the clear, concise explanation of where you will play and how you will win. Without it, you're just another fund asking for money.

Validating Your Angle with Market Research

Once you’ve got a working hypothesis, you need to beat it up with serious market research. The point isn't to confirm what you already believe; it's to pressure-test your idea against the harsh realities of the market. You're looking for hard data that proves your niche is both underserved and packed with opportunity.

Your research needs to answer some tough questions:

- Market Size: Is this pond big enough to generate the returns your LPs are expecting?

- Competitive Landscape: Who are you up against? What are their track records, and how is your strategy genuinely different?

- Deal Flow Potential: Can you realistically find enough quality deals to put your capital to work?

- Exit Opportunities: What’s the endgame? Are there clear paths to liquidity, like acquisitions or IPOs in your target sector?

Let’s say your thesis is early-stage fintech in Latin America. Your research would mean digging into startup formation rates, tracking regulatory shifts, and mapping out every incumbent VC in the region. You’d need to get on the phone with local founders and angel investors to get a feel for the real-world dynamics.

This is the unglamorous groundwork that gives you the proof points for a compelling business plan. For a complete picture, a guide on how to start an investment firm from the ground up can offer an invaluable end-to-end perspective. Honestly, this research and planning phase is the most critical part of building a firm that doesn't just launch, but actually lasts.

Navigating the Legal and Regulatory Path

Once you’ve nailed down a sharp investment thesis, the next leg of the journey is less about big ideas and more about a solid foundation. Launching an investment company is, at its core, a legal and regulatory marathon. Any missteps here can stop your firm before it even gets off the ground.

This is where you build the legal fortress that protects you, your partners, and your investors. Getting this part right isn't optional—the decisions you make now, from business structure to compliance filings, will dictate how you operate for years to come.

Choosing Your Legal Structure

First things first: you need to decide on the legal entity for your firm. This isn't just about checking a box on a form; it directly impacts your personal liability, how you're taxed, and the way you distribute profits down the line.

The two most common choices are a Limited Liability Company (LLC) or a corporation.

- Limited Liability Company (LLC): This is the go-to for most new fund managers, and for good reason. An LLC offers pass-through taxation, which means profits and losses are passed directly to the members. This setup helps you avoid the "double taxation" that corporations often face. Crucially, it also provides a liability shield, separating your personal assets from the firm's debts.

- Corporation (C-Corp or S-Corp): A more formal structure that might make sense if you plan to seek venture capital for your management company itself or want to offer stock options. But be aware, C-Corps face corporate taxes on profits, and then shareholders get taxed again on dividends.

For most emerging managers, an LLC hits the sweet spot between protection and operational simplicity. It lets you focus on what you do best—managing investments—without getting bogged down in the complex governance required of a corporation.

Demystifying Regulatory Registration

With your entity formed, you're ready to step into the world of regulatory oversight. In the United States, the main player is the Securities and Exchange Commission (SEC). Whether you need to register with them hinges on a few key factors, primarily your Assets Under Management (AUM) and the number of investors you bring on.

Launching an investment company requires significant capital and a clear path through regulatory hoops. Globally, founders typically start by registering a business structure, like an LLC, and then work with the relevant authorities.

Here in the U.S., a firm must register with the SEC under the Investment Company Act of 1940 if it manages over $150 million in assets or has 100 or more investors. The initial capital needed can be substantial, as many venture funds aim for $10 million to $100+ million in their first raise.

The good news? If you're just starting out and fall below these thresholds, you might qualify for a lighter registration.

Many new fund managers can operate as an Exempt Reporting Adviser (ERA). This status has far less burdensome reporting requirements than a fully registered adviser, though you still need to file with the SEC and comply with state rules.

Figuring out which category you fall into is absolutely critical. A misstep here can lead to serious penalties. For a detailed breakdown, our guide on the topic is a must-read: https://www.fundpilot.app/blog/exempt-reporting-advisers-key-compliance-guide.

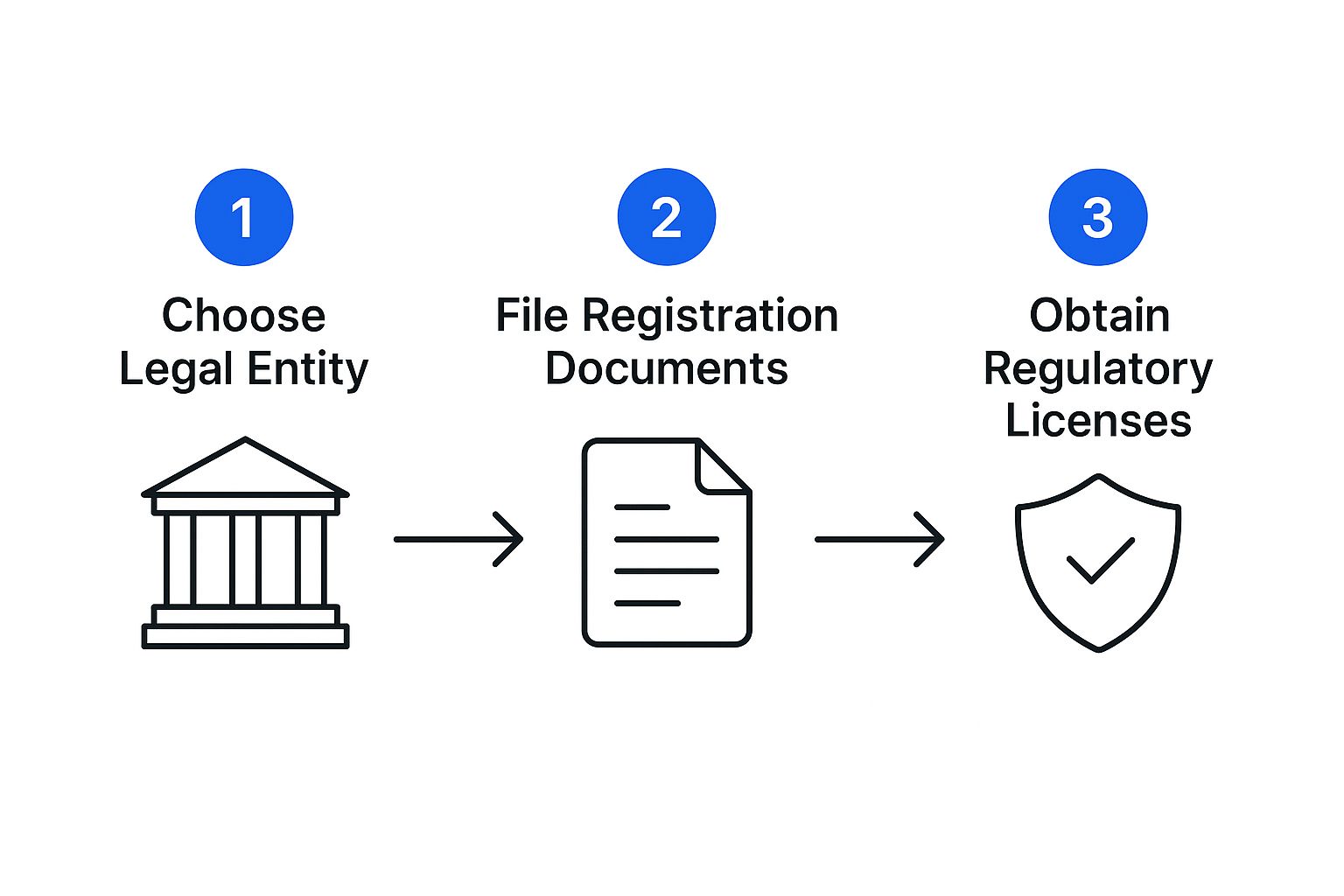

The entire process of getting your investment company legally registered follows a clear, step-by-step path.

As the visual shows, each step builds on the last. A methodical approach isn't just recommended; it's essential.

To help clarify this journey, here's a look at the key milestones you'll encounter.

Key Regulatory Milestones for a New Investment Firm

| Milestone | Description | Key Considerations |

|---|---|---|

| Entity Formation | Legally creating your management company, typically as an LLC or corporation. | Impacts liability, taxation, and operational flexibility. An LLC is often the preferred choice for new managers. |

| EIN Application | Obtaining an Employer Identification Number from the IRS for tax purposes. | This is a straightforward but mandatory step for opening bank accounts and filing taxes. |

| Regulatory Analysis | Determining your registration status with the SEC and state authorities. | Are you an RIA or an ERA? This depends on your AUM, number of investors, and investment strategy. |

| Form ADV Filing | The official registration document filed with the SEC or state regulators. | Part 1 is public, while Part 2 (the "brochure") is given to clients and LPs. It must be accurate and updated annually. |

| Licensing | Ensuring key personnel hold required licenses, like the Series 65. | Requirements vary by state and registration status. Some exemptions may apply. |

| Ongoing Compliance | Establishing an internal compliance program to meet all regulatory obligations. | This includes a code of ethics, custody rules, marketing material reviews, and annual updates. |

Navigating these steps correctly from the start will save you from major headaches and potential regulatory issues later on.

Your Shield: Essential Legal Documents

With your structure in place and your registration path clear, it's time to draft the core documents that will govern your fund. These aren't just formalities; they are the legally binding contracts that protect you and your investors.

Here are the non-negotiables:

- Private Placement Memorandum (PPM): Think of this as your fund's primary disclosure document. It spells out your investment strategy, the risks involved, your team's background, and the terms of the investment. A well-written PPM is your best defense against future disputes.

- Limited Partnership Agreement (LPA): This is the legal rulebook for the relationship between you (the General Partner) and your investors (the Limited Partners). It covers critical terms like management fees, carried interest, capital calls, and how profits get distributed.

- Subscription Agreement: This is the contract an investor signs to officially commit capital to your fund. It confirms they've received and understood both the PPM and the LPA.

When you're setting up, you'll need to prepare several of these foundational legal papers. For a broader look at the paperwork involved, this guide on essential legal documents for startups is a great resource.

My best advice? Don’t try to do this yourself. Work with experienced legal counsel who specializes in fund formation. Getting these documents airtight from day one will save you an incredible amount of trouble down the road.

Securing Capital and Building Investor Trust

You can have the sharpest investment thesis and a bulletproof legal structure, but without capital, your fund is just an idea on paper. Fundraising is where the rubber meets the road. It’s often the toughest—and most humbling—part of launching a new firm.

This isn’t just about asking for money. It's about finding the right Limited Partners (LPs) who genuinely buy into your vision for the long haul. You have to tell a story that connects, with a pitch that does more than just present numbers—it has to sell conviction in your ability to execute.

Identifying and Connecting with the Right LPs

Your first real task in fundraising is building a smart, targeted list of potential LPs. The keyword here is alignment. A scattergun approach of blasting your deck to every investor you can find is a rookie mistake. It burns bridges and wastes precious time.

Instead, think strategically about who you're approaching:

- Family Offices: These investors are often more nimble and can make decisions faster than large institutions. They're also sometimes more receptive to a unique founder story or a niche strategy that doesn't fit neatly into a big-firm mandate.

- High-Net-Worth Individuals (HNWIs): Often sourced through your personal and professional network, HNWIs can be the perfect partners for your first close. Getting them on board creates the momentum you need to attract others.

- Institutional Investors: This is the world of pension funds, endowments, and foundations. They can write big checks, but be prepared for a far more grueling due diligence process with much longer timelines.

In my experience, the most successful fundraising comes from warm introductions. Tap into your network—old colleagues, alumni from your university, industry contacts—to get a direct line to the decision-makers. A cold email has a slim chance, but a referral from a trusted source gives you instant credibility.

The funding world is always shifting, and you need to know the landscape you're playing in. The global VC market, for instance, has seen massive rounds, especially in hot sectors like AI and fintech. While corporate-backed funding is on the rise, early-stage investment is still the lifeblood of innovation. Today, seed rounds typically fall between $500,000 and $2 million, while Series A rounds are now averaging around $15 million, a sign of higher valuations and fierce competition for the best deals.

Crafting a Pitch Deck That Sells a Story

Your pitch deck is your ambassador—it gets into rooms you can't. It needs to be incredibly clear, concise, and compelling. Remember, investors are drowning in decks. Yours has to cut through the noise by telling a coherent, believable story about why your firm needs to exist.

A winning pitch deck usually flows through these key elements:

- The Opportunity: Why now? Pinpoint the market gap or inefficiency your fund is designed to exploit.

- Your Unique Thesis: In plain language, what’s your strategy? What’s your edge that others don't have?

- The Team: This is critical. Showcase your team's track record and deep, relevant experience. Why are you the only ones who can win with this strategy?

- Deal Sourcing: How will you find unique investment opportunities that aren't on everyone else's radar?

- Fund Structure and Terms: Be transparent about management fees, carried interest, and other key terms.

- Case Studies: If you have them, show examples of past investments. Nothing proves your acumen like a track record.

If you’re getting ready to hit the fundraising trail, this guide on how to raise startup capital offers some great practical advice to sharpen your approach.

Navigating Due Diligence and Building Trust

Once an investor shows interest, get ready for the deep dive. The due diligence process is intense. They will comb through everything—your legal docs, your operational setup, your investment models. This is where transparency is everything.

This is also where real trust is built. Answer every question directly. Be upfront about what you don't know and show that you have a firm grasp of the risks. Investors are ultimately backing people, not just a strategy. They need to believe that you're a credible and responsible steward for their capital.

That trust doesn't end when the check is signed. It's an ongoing commitment that becomes the foundation of investor relations. It’s about clear, consistent communication—not just when you have good news, but especially when markets get choppy. To learn more, take a look at our guide on https://www.fundpilot.app/blog/what-is-investor-relations-a-guide-for-fund-managers. In the end, finding the right partners for the long journey is worth far more than just taking the first check that comes your way.

Building Your Firm's Operational Backbone

Once you've navigated the legal maze and secured your initial capital, it's time to build the engine room of your firm. This is where the real work begins. We're talking about the day-to-day operations—the systems and people that will keep your fund running smoothly. Get this right, and you'll build investor confidence and free yourself up to focus on what you do best: generating returns.

A breakdown in operations is one of the fastest ways a new fund can stumble. Your operational backbone really comes down to three things: who you partner with, the technology you use, and how you manage compliance. Let's dig into each.

Assembling Your Team of Key Partners

You can't do this alone. A successful investment firm relies on a network of specialized service providers who handle critical functions you shouldn't be doing yourself. Think of these partners less as vendors and more as an extension of your own team.

Here are the non-negotiables:

- Fund Administrator: This is probably your most critical operational partner. They’re the ones handling the heavy lifting on accounting, calculating your Net Asset Value (NAV), managing capital calls and distributions, and preparing the financial statements your LPs will receive. A top-notch administrator provides independent, third-party validation of your numbers, which is absolutely essential for building trust.

- Auditor: Every year, you'll need an independent auditor to go through your fund's financials with a fine-tooth comb. They verify that everything is accurate and complies with accounting standards. For institutional LPs, a clean audit opinion isn't just nice to have—it's a requirement.

- Prime Broker: If you're trading public securities (think hedge funds), your prime broker is the central nervous system for all your trading activity. They handle everything from custody of your assets and trade execution to securities lending.

When you're vetting these partners, don't just look at the price. Ask for references, specifically from other emerging managers. You need to know if they understand your strategy and if they have the capacity to grow with you.

A classic rookie mistake is trying to DIY the back office to save a few bucks. It's a false economy. Outsourcing administration and audit functions to reputable firms not only lets you focus on investing but also sends a clear signal to LPs that you're running an institutional-grade operation from day one.

Building a Modern and Scalable Tech Stack

The days of running a multi-million dollar fund from a few spreadsheets are long gone. The right tech stack doesn't just make you more efficient; it gives you a serious analytical edge and provides the professional polish investors now expect.

Your foundational tech should cover three core areas:

- Portfolio Management Software: This is your command center. It's where you track investment performance, monitor your exposure, and run "what-if" scenarios. You need a real-time, at-a-glance view of your portfolio's health.

- Investor Portal: A secure, branded portal is now table stakes. This is where your LPs can log in to see their statements, find key documents, and get performance updates. It saves you an incredible amount of administrative time fielding one-off requests.

- CRM System: You need a central place to manage your pipeline of potential deals and track every interaction with your LPs. A good CRM ensures that crucial relationship intelligence isn't lost in someone's inbox.

Investing in the right tools will make you a better investor, full stop. Good data helps you spot trends, identify risks, and make smarter decisions.

Establishing Robust Compliance and Risk Management

Finally, you need to wrap this entire operational structure in a rock-solid compliance and risk management framework. This isn't just about keeping regulators happy; it's about protecting your investors, your reputation, and your firm.

Your first step is to create a detailed Compliance Manual. Think of this as the official rulebook for your firm. It should clearly outline your policies on everything from the code of ethics and personal trading to cybersecurity protocols.

Clean financial records are the bedrock of good compliance. To get this right from the start, following a comprehensive guide to bookkeeping for startups can be a lifesaver. It helps you establish a clean, auditable trail from the moment you launch.

Beyond that, you need a process for managing risk. This means proactively identifying anything that could threaten your strategy—market volatility, operational glitches, or sudden regulatory shifts—and having a clear plan to deal with it. Showing investors you're a prudent steward of their capital is how you build a firm that lasts.

Deploying Capital and Managing Your Portfolio

You’ve got the legal side buttoned up and the capital is in the bank. Now the real work starts. Getting the fund launched is just the first lap; the race is won by delivering on the promises you made to your investors. This whole phase is about one thing: the disciplined, day-in-day-out execution of your investment strategy.

Success from here on out isn't just about cutting checks. It’s about sniffing out proprietary deals that others miss, digging deep with due diligence to find the risks nobody's talking about, and actively managing your portfolio companies to create real, measurable value. This is where your investment thesis goes from a slide deck to a track record.

Sourcing and Executing Deals

Finding truly unique investment opportunities is what separates the top-tier funds from the rest of the pack. If you're only seeing the same deals that every other firm is looking at, you're setting yourself up for overpaying and underperforming. To build a portfolio that actually stands out, you need to cultivate your own proprietary deal flow.

This comes down to building real, deep relationships within your chosen niche. Let's say you're running an early-stage venture fund. That might mean:

- Hanging out at university incubators: You want to find brilliant founders long before they hit the typical fundraising circuit.

- Building a network of specialized lawyers and accountants: These professionals are often the first to know when a promising company is getting serious about its future.

- Becoming a true thought leader: Get on stage at industry events and publish content that's genuinely insightful. You want to be the first person entrepreneurs think of when they're ready to make a move.

Once a promising opportunity lands on your desk, your due diligence has to be relentless. This isn't just a financial audit. It's a full 360-degree investigation into the business, the market it lives in, and, most importantly, its leadership team. You're searching for the story that isn't in the pitch deck—the operational cracks or the competitive threats lurking just out of sight.

Active Portfolio Management and Support

Your work isn’t done when the wire transfer hits their account. Honestly, it's just getting started. Active portfolio management means you're rolling up your sleeves and genuinely helping your companies win. It's a tricky balance—you need to provide support and guidance without ever crossing the line into micromanagement.

Effective portfolio management really breaks down into three key areas:

- Strategic Guidance: You're there to offer board-level advice on the big stuff—product strategy, critical hires, and of course, future fundraising rounds.

- Network Access: Your Rolodex is one of your most valuable assets. Open it up and connect your founders with potential customers, strategic partners, and top-tier talent.

- Performance Monitoring: Set clear key performance indicators (KPIs) from the start and hold the management team accountable through regular, structured check-ins.

This hands-on approach does more than just protect your capital; it can dramatically increase the value of your investment. It also gives you the ground-level intelligence you need when it's time to make the hard decisions, like participating in a follow-on round or engineering an exit.

Your relationship with your portfolio companies should be a partnership, not a transaction. The value you bring beyond your capital is what separates good investors from great ones.

Mastering Investor Relations

Finally, while you're busy managing your investments, you have another critical job: managing your investors. Nothing builds long-term trust more effectively than consistent, transparent communication. Your Limited Partners gave you their capital based on trust; they absolutely deserve to know how their investment is doing.

This means providing regular, genuinely insightful updates—and not just glossy reports when everything is going perfectly. Be upfront about the challenges and, more importantly, what you're doing to tackle them. When the market gets choppy, proactive communication is your single best tool for calming nerves and reinforcing the long-term vision. Showing that steady hand is a core part of learning how you start an investment company that is truly built to last.

Common Questions from New Founders

Once you’ve wrestled with your strategy and waded through the initial legal paperwork, the real-world questions start to hit. You’re past the theoretical stage, and now it’s about money, people, and avoiding the mistakes that have sunk other new managers.

Let’s get into the nitty-gritty. Answering these questions head-on will help you set a realistic budget, assemble the right team, and sidestep the landmines that others have stepped on.

How Much Money Do I Really Need to Get Started?

This is the million-dollar question, and the answer truly depends on the kind of firm you're building. If you're launching a straightforward advisory business, you might be able to get it off the ground with less than $100,000 for initial operating costs.

But for a venture capital or private equity fund where you're investing directly, the math is entirely different. You need enough working capital to cover everything—formation costs, legal bills, compliance, salaries, rent—for at least the first two years. This is your "management company" budget, and it's completely separate from the capital you raise from Limited Partners (LPs).

Realistically, you should budget anywhere from $250,000 to over $1 million for this initial runway. To put that in perspective, a small "micro-VC" fund often aims to secure at least $10 million in AUM in its first close just to make the economics work.

Can I Start an Investment Firm Without a Finance Background?

It's a tough road, but I've seen it done successfully. The trick is to be brutally honest about your weaknesses and build a team that makes them irrelevant.

Say you're a biotech Ph.D. with incredible domain expertise in life sciences. Your value isn't your financial modeling skill; it's your ability to see what others miss in the lab. For this to work, you absolutely must bring on co-founders who live and breathe fund management, compliance, and financial operations.

Don't underestimate this. Both investors and regulators will put your team's collective resume under a microscope. You have to prove you have a credible, verifiable track record in your niche, even if your part of that track record isn't purely financial.

What Are the Biggest Mistakes New Firms Make?

Knowing where others have failed is your best defense. While every fund launch has its own unique drama, a few classic mistakes pop up over and over again. If you can get ahead of these, you're already in a much stronger position.

I see four pitfalls that consistently trip up new investment managers:

- Underestimating the Regulatory Burden: This is the big one. A mistake in your registration or a failure in ongoing compliance isn't just a slap on the wrist. It can lead to massive fines, a ruined reputation, or even regulators shutting you down for good.

- Ignoring the Back Office: It's easy to get caught up in the thrill of fundraising and deal-making. But if you neglect the unsexy work of fund administration, reporting, and compliance, you're building on a foundation of sand. It will catch up to you.

- A Fuzzy Investment Thesis: If you can't articulate your strategy in a clear, compelling way, sophisticated LPs won't give you the time of day. A generic approach gets you nowhere—you'll be lost in the crowd, unable to attract capital or find unique deals.

- Bad Investor Communication: This erodes trust faster than anything else. You have to be transparent and consistent with your updates, especially when things aren't going well. Strong LP relationships are built on honesty, not just a highlight reel.

Navigating these challenges is a core part of learning how you start an investment company that can actually survive and thrive for the long haul.

Ready to move beyond spreadsheets and operate like an institutional-grade firm? Fundpilot empowers emerging managers with professional LP reporting, a secure investor portal, and automated fund administration. Streamline your operations, build investor trust, and focus on what matters most—sourcing deals and raising capital. Discover how Fundpilot can accelerate your growth.