Your 2025 Financial Audit Checklist: 7 Essential Steps

Master your next audit with our comprehensive financial audit checklist. Explore 7 key steps for a seamless and compliant review process in 2025.

A financial audit can feel like a daunting, high-stakes examination. Yet, with the right preparation, it transforms into a valuable opportunity to validate financial health, uncover operational efficiencies, and strengthen stakeholder confidence. For emerging fund managers and growing businesses, a smooth audit is not just about compliance; it is a cornerstone of building institutional credibility and attracting investment. This comprehensive financial audit checklist breaks down the entire process into manageable, high-impact focus areas, turning a complex requirement into a clear roadmap for success.

We will move beyond generic advice, providing you with actionable steps, real-world examples, and specific documentation you need to gather for each stage of the audit. Think of this as more than just a list. It is a strategic guide designed to help operations teams, compliance officers, and fund managers proactively organize their financial records. By following this guide, you can shift your audit from a stressful obligation to a strategic asset, ensuring your records are not just correct, but truly audit-ready.

This article specifically focuses on the core financial components, but a successful audit often begins with broader organizational readiness. For a comprehensive guide on readying your entire organization for any type of audit, you might find our ultimate audit preparation checklist to be an invaluable resource. Now, let’s dive into the seven critical financial areas you need to master.

1. Review and Test Internal Controls

A financial audit checklist is incomplete without a rigorous evaluation of your organization's internal controls. This foundational step involves assessing the design and operational effectiveness of the policies and procedures management has established. Strong internal controls are the bedrock of reliable financial reporting, operational efficiency, and regulatory compliance, acting as the first line of defense against fraud and error.

The process is not just about ticking boxes; it's a deep dive into how your company safeguards assets, authorizes transactions, and maintains accurate records. Auditors examine everything from segregation of duties, where no single individual has control over all aspects of a financial transaction, to the automated systems governing revenue recognition. The infamous 2016 Wells Fargo scandal, where control failures led to fraudulent accounts, serves as a stark reminder of the critical importance of this process. A thorough review ensures that the controls you have on paper are functioning effectively in practice.

A Systematic Approach to Control Testing

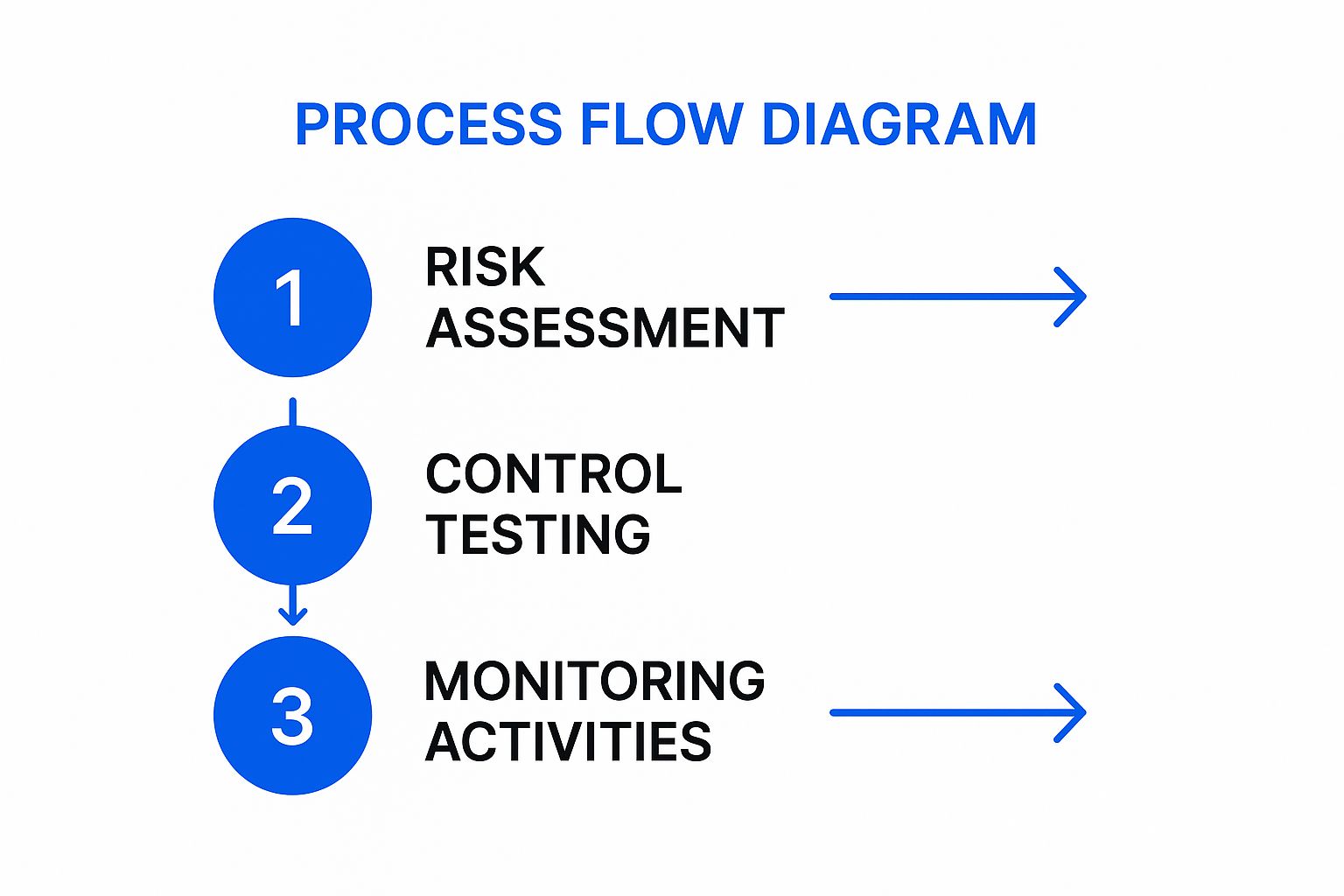

To effectively test internal controls, auditors and finance teams must adopt a structured, risk-based methodology. This ensures that the most critical areas of the business receive the most attention, optimizing audit resources and maximizing effectiveness.

The following infographic illustrates the cyclical, three-step process for a systematic evaluation of internal controls.

This process flow highlights that effective control evaluation is an ongoing cycle, not a one-time event, starting with identifying risks and culminating in continuous monitoring for sustained compliance.

Actionable Tips for Implementation

To make this a practical part of your financial audit checklist, consider these strategies:

- Adopt a Risk-Based Approach: Begin by identifying and prioritizing high-risk areas. For a fund manager, this might be the valuation of complex portfolio assets or the process for capital calls and distributions. Focus your initial testing efforts here.

- Document Everything: Meticulously document any control deficiencies you find. Your report should include the specific control that failed, the potential impact, and clear, actionable recommendations for remediation.

- Test Throughout the Period: Don't wait until year-end. Conduct interim testing on controls throughout the audit period. This provides a more accurate picture of their effectiveness and allows for timely correction of issues.

- Collaborate with IT: Modern controls are often automated and embedded within complex IT systems. Coordinate with IT specialists or auditors to properly test application controls, system access rights, and data integrity protocols.

By proactively reviewing and testing your internal controls, you not only prepare for a smoother audit but also strengthen your organization's overall governance and risk management framework. For more guidance on structuring your review, you can find valuable insights on how to build a better internal audit checklist template.

2. Cash and Bank Reconciliation Verification

A cornerstone of any financial audit checklist is the rigorous verification of cash and bank reconciliations. This process confirms one of the most liquid and susceptible assets an organization holds: cash. It involves a detailed examination of cash balances, bank statements, and the reconciliations that tie them together to ensure accuracy, completeness, and the proper cutoff of cash transactions. Strong cash verification procedures are vital for detecting misstatements, preventing fraud, and ensuring the company's reported cash position is reliable.

The goal is to substantiate the cash balance reported on the balance sheet. Auditors achieve this by independently confirming balances directly with financial institutions and meticulously scrutinizing the reconciling items, such as outstanding checks and deposits in transit. This step is critical because cash is universally high-risk. A famous example is the early 2000s Enron scandal, where complex and often misleading cash management structures were used to hide debt and inflate earnings, underscoring the need for auditors to perform extensive bank confirmation and reconciliation procedures.

A Systematic Approach to Cash Verification

To effectively audit cash, a methodical approach is necessary. This involves more than just agreeing on a number; it requires understanding the entire cash management process, from receipts to disbursements, and verifying the integrity of the reconciliation process itself. This systematic evaluation confirms that recorded cash exists and that all cash transactions for the period have been recorded correctly.

The following process provides a clear framework for conducting a thorough verification of cash and bank balances, ensuring all key assertions are addressed.

- Direct Confirmation with Banks: The auditor sends confirmation requests directly to all banks where the company holds accounts. This provides independent, third-party verification of year-end balances, loan amounts, and any other relevant financial arrangements.

- Reconciliation Testing: Auditors obtain the company’s bank reconciliations for all accounts and re-perform the reconciliation. This involves agreeing the bank balance to the confirmation, tracing reconciling items to subsequent bank statements, and verifying the mathematical accuracy of the reconciliation.

- Cutoff Analysis: This crucial step involves examining transactions occurring a few days before and after the fiscal year-end. The goal is to ensure that transactions are recorded in the correct accounting period, preventing the manipulation of cash balances.

This structured procedure ensures that the cash balance is not only mathematically correct but also fairly presented in the context of the company's overall financial position.

Actionable Tips for Implementation

To integrate this verification process into your financial audit checklist effectively, consider these practical strategies:

- Perform Bank Confirmations Early: Initiate the bank confirmation process as of the balance sheet date. Sending these requests early ensures you receive responses from financial institutions in a timely manner, preventing delays in the audit process.

- Independently Verify Reconciling Items: While you will review the bank reconciliations prepared by your client, it's crucial to independently verify the significant reconciling items. For outstanding checks, trace them to the subsequent month’s bank statement to confirm they cleared. For deposits in transit, verify they were credited by the bank in the following period.

- Scrutinize Unusual Items: Pay special attention to large, old, or unusual reconciling items. An outstanding check that has not cleared for several months could indicate a recording error or a potential liability issue that needs to be investigated.

- Test Interbank Transfers at Year-End: For organizations with multiple bank accounts, like a multinational corporation managing cash globally, test bank transfers around the year-end for proper cutoff. This helps detect "kiting," a fraudulent scheme where cash is recorded in two places at once.

3. Revenue Recognition and Cutoff Testing

A crucial component of any financial audit checklist is the rigorous examination of revenue recognition and cutoff procedures. This step focuses on verifying that revenue transactions are recorded in the correct accounting period and measured accurately according to standards like ASC 606. Improper revenue recognition is a leading cause of financial restatements, making this area a high-risk focus for auditors.

The process involves more than just matching invoices to payments; it's a deep dive into the specifics of contracts and performance obligations. Auditors scrutinize whether revenue is recognized when control of goods or services is transferred to the customer, not just when cash is received. The infamous Xerox accounting scandal in the early 2000s, where the company prematurely booked revenue from long-term leases, underscores the severe consequences of getting this wrong. A thorough review ensures revenue is not overstated in the current period or understated to manipulate future earnings.

A Systematic Approach to Revenue Testing

To effectively audit revenue, finance teams and auditors must employ a structured methodology that addresses timing (cutoff), measurement, and presentation. This approach ensures that the audit procedures are comprehensive and specifically target the areas most susceptible to misstatement, as dictated by the complexity of the company's revenue streams.

This systematic process involves verifying transaction details against underlying contracts, assessing the timing of revenue recognition around the period-end, and confirming compliance with applicable accounting frameworks. This structured verification is essential for providing assurance over the accuracy of the most critical figure on the income statement.

Actionable Tips for Implementation

To make revenue testing a practical and effective part of your financial audit checklist, consider these strategies:

- Focus on Complex Contracts: Prioritize contracts with multiple performance obligations, such as a software company like Salesforce that bundles subscriptions with implementation and support services. Each obligation must be identified and have its revenue allocated and recognized separately.

- Perform Cutoff Testing: Select a sample of revenue transactions recorded just before and immediately after the fiscal year-end. Trace these back to shipping documents, service delivery confirmations, and customer contracts to confirm they are recorded in the correct period.

- Review Subsequent Period Adjustments: Scrutinize credit memos, sales returns, and other adjustments made after the period-end. A high volume of returns related to pre-year-end sales could indicate aggressive revenue recognition practices or channel stuffing.

- Analyze Unusual Terms: Pay close attention to contracts with non-standard terms, such as extended payment options, side agreements, or significant financing components. These complexities can significantly impact the timing and amount of revenue to be recognized.

By systematically testing revenue recognition and cutoff, you validate the accuracy of your reported performance and strengthen investor confidence in your financial statements. For those navigating complex revenue streams, understanding the nuances of fund accounting vs. corporate accounting can provide valuable context for these critical audit areas.

4. Accounts Receivable and Allowance Analysis

A crucial component of any financial audit checklist is the rigorous examination of accounts receivable (AR) and the corresponding allowance for doubtful accounts. This step involves more than just verifying outstanding balances; it's a critical assessment of an asset's collectibility and the reasonableness of management's estimates. An accurate AR valuation is fundamental to presenting a true and fair view of a company's financial health, directly impacting reported revenue and net income.

Auditors delve into the processes for granting credit, invoicing customers, and collecting payments to evaluate the overall health of the receivables portfolio. This scrutiny ensures that the balance sheet doesn't overstate assets with amounts that are unlikely to be collected. For instance, a healthcare organization must meticulously manage complex insurance and patient receivables, where collection rates can vary dramatically. Failure to properly estimate uncollectible accounts can materially misstate financial results, undermining investor confidence and regulatory compliance.

A Systematic Approach to AR Validation

To effectively audit accounts receivable, auditors must employ a structured methodology that combines direct confirmation, analytical procedures, and a detailed review of aging schedules. This ensures that the recorded receivables are valid, accurate, and likely to be converted into cash.

The evaluation process typically follows a clear path from confirming existence to assessing valuation. This involves verifying balances directly with customers, analyzing historical collection patterns, and stress-testing the assumptions used to calculate the allowance for credit losses. This systematic review provides comprehensive assurance over one of the most significant assets on the balance sheet.

Actionable Tips for Implementation

To make this a practical part of your financial audit checklist, consider these strategies:

- Review Subsequent Cash Collections: One of the most effective ways to validate year-end receivable balances is to examine cash receipts from customers in the period immediately following the year-end. Strong subsequent collections provide powerful evidence that the receivables existed and were collectible.

- Analyze Changes in Allowance Rates: Compare the current year's allowance for doubtful accounts as a percentage of total receivables to historical patterns and industry benchmarks. Any significant deviations should be investigated and justified based on changes in customer base, credit policies, or economic conditions.

- Stratify and Test Aging Reports: Don't treat all receivables equally. Stratify the AR aging report by customer, size, and age. Focus confirmation procedures and detailed testing on large, overdue, or unusual balances, which carry the highest risk of misstatement. For a large, diverse portfolio, consider using statistical sampling for confirmations.

- Evaluate Economic and Industry Factors: The allowance for credit losses shouldn't be calculated in a vacuum. Consider macroeconomic trends, industry-specific challenges, and the financial health of key customers. For example, a downturn in the retail sector should prompt a more conservative estimate for uncollectible accounts from retail clients.

By systematically analyzing your accounts receivable and the adequacy of your allowances, you ensure the integrity of your reported earnings and provide stakeholders with a reliable picture of your company's liquidity and operational effectiveness.

5. Inventory Valuation and Physical Count Verification

For companies holding physical goods, the inventory line item on the balance sheet is often one of the most significant assets. A crucial component of any financial audit checklist is the verification of inventory quantities and the assessment of its valuation. This process goes beyond simply agreeing on numbers; it involves physically observing inventory counts, testing the costing methods used (like FIFO or weighted average), and ensuring the inventory is valued correctly according to accounting standards.

This step is vital for confirming that the asset is not materially misstated, either through inaccurate counts or improper valuation. Auditors must scrutinize the entire process to guard against overstatement of assets and understatement of expenses. For example, automotive companies like Ford rely on precise just-in-time inventory systems where even small discrepancies can signal significant operational or financial issues. A robust verification process provides assurance to stakeholders that the reported inventory value is both accurate and fairly presented.

A Systematic Approach to Inventory Verification

To effectively audit inventory, both the physical existence and its carrying value must be substantiated. This requires a structured methodology that combines direct observation with detailed analytical testing. Auditors and management must work together to ensure the process is efficient, comprehensive, and minimizes disruption to daily operations.

This approach ensures that every angle is covered, from the physical items on the shelves to the complex calculations that determine their financial value. It addresses the core risks associated with inventory: existence, completeness, and valuation.

Actionable Tips for Implementation

To make inventory verification a smooth part of your financial audit checklist, consider these practical strategies:

- Plan Observations in Advance: Coordinate with the client well ahead of the physical count. Understand their procedures, locations, and timing. This preparation is key to a successful observation and avoids last-minute complications.

- Analyze for Obsolete Inventory: Pay close attention to items that are slow-moving, near expiration, or potentially obsolete. Pharmaceutical companies, for instance, must rigorously track expiration dates. These items may require a write-down to their net realizable value.

- Test Inventory Cutoff: Verify that transactions around the year-end are recorded in the correct period. Review shipping and receiving documents for several days before and after the count date to ensure sales and purchases are not improperly shifted between periods.

- Leverage Technology: To effectively manage inventory and ensure accurate counts and valuation, explore using the best inventory management software. These tools can automate tracking, improve count accuracy, and provide valuable data for auditors.

By systematically verifying both the physical count and the valuation method, you provide strong evidence supporting one of the most material assets on the balance sheet. For further reading on asset valuation principles, you can gain more insights from this guide to the valuation of private company assets.

6. Fixed Assets and Depreciation Analysis

A comprehensive financial audit checklist must include a detailed review of an organization’s fixed assets and related depreciation. This step involves examining the lifecycle of property, plant, and equipment (PP&E), from acquisition and capitalization to depreciation and eventual disposal. Proper management and accounting for these long-term assets are crucial for accurately reflecting a company's financial health, as they often represent a significant portion of the balance sheet.

This is not a simple inventory count; it's a deep dive into the policies and calculations that govern these substantial investments. Auditors scrutinize whether asset additions are capitalized correctly, if depreciation methods are applied consistently and are appropriate for the asset type, and if disposals are recorded accurately. For asset-intensive industries, this process is paramount. For example, an airline like Delta must meticulously manage aircraft depreciation schedules and maintenance reserves, while technology firms must properly evaluate the capitalization of software development costs. A thorough review ensures that asset values are not overstated or understated, preventing material misstatements.

A Systematic Approach to Asset Verification

To effectively audit fixed assets, finance teams and auditors need a structured methodology that covers acquisition, valuation, and disposal. This ensures all facets of the asset lifecycle are examined for accuracy, compliance with accounting standards, and consistency with prior periods.

This systematic verification process ensures that the physical existence, valuation, and accounting treatment of fixed assets are rigorously tested, providing confidence in the figures presented on the financial statements.

Actionable Tips for Implementation

To integrate this critical step into your financial audit checklist, consider these practical strategies:

- Review Board Minutes: Scrutinize the minutes from board of directors meetings for approvals of major capital expenditures. This helps verify the authorization and business purpose behind significant asset acquisitions.

- Test a Sample of Additions: Select a sample of new fixed assets and trace them back to supporting invoices and capitalization policies. This confirms that costs are recorded correctly and that only appropriate expenditures are capitalized.

- Verify Depreciation Consistency: Confirm that the depreciation methods (e.g., straight-line, declining balance) and useful life estimates are consistent with those used in previous years. Any changes must be justified and properly disclosed.

- Assess for Impairment: Consider external and internal economic indicators that might suggest asset impairment. This could include significant market declines, technological obsolescence, or physical damage that reduces an asset's value.

- Review Insurance Coverage: Examine the company's insurance policies to ensure that fixed assets are adequately covered. The insured values can sometimes serve as a secondary indicator of the assets' fair market value.

By diligently analyzing fixed assets and depreciation, you safeguard the integrity of your balance sheet and provide stakeholders with a true and fair view of the company's operational base. For fund managers dealing with portfolio companies that have significant fixed assets, understanding these nuances is essential. You can find more detailed guidance on handling complex asset structures by mastering private equity accounting.

7. Debt and Interest Expense Verification

A crucial element of any comprehensive financial audit checklist involves the meticulous verification of debt obligations and related interest expenses. This process goes beyond simply agreeing balances to statements; it's a deep-seated examination of all borrowings, including bank loans, bonds, convertible notes, and lines of credit. The primary goal is to ensure that liabilities are completely and accurately reported and that the associated interest expenses and financing costs are correctly calculated and recognized in the proper period.

Misstating debt can have a significant ripple effect across the financial statements, impacting key metrics like leverage ratios, solvency, and profitability. Auditors scrutinize these areas closely because debt agreements often contain complex terms and covenants that can affect a company's financial health and operational freedom. For instance, Tesla's use of convertible bonds involves complex accounting for embedded derivative features, which requires specialized knowledge to audit correctly. A thorough review in this area provides stakeholders with confidence that the company's financial obligations are transparently and accurately disclosed.

A Systematic Approach to Debt Verification

To effectively audit debt and interest, both finance teams and auditors should follow a structured approach that confirms existence, completeness, valuation, and disclosure. This method ensures all aspects of debt accounting, from initial recognition to covenant compliance, are thoroughly vetted.

The process involves obtaining independent confirmations, analyzing agreements for critical terms, recalculating expenses and amortization schedules, and ensuring compliance with all contractual obligations. This systematic verification prevents surprises and ensures the financial statements present a true and fair view of the company’s liabilities.

Actionable Tips for Implementation

To integrate this verification process into your financial audit checklist effectively, consider these practical strategies:

- Obtain Direct Confirmations: Proactively request and reconcile confirmations directly from all lenders, trustees, and creditors. These documents should detail principal balances, accrued interest, payment terms, and any pledged collateral. This provides independent, third-party evidence of the obligations.

- Scrutinize Debt Agreements: Review all loan agreements, bond indentures, and credit facility contracts in detail. Identify and summarize key terms, including interest rates, maturity dates, prepayment penalties, and restrictive covenants. Pay special attention to any complex features or clauses.

- Test Covenant Compliance: Independently recalculate all financial covenant ratios (e.g., debt-to-equity, interest coverage) as stipulated in the agreements. Document the calculations and evidence of compliance for the audit period. This is especially critical for real estate companies managing multiple construction loans with specific performance hurdles.

- Verify Proper Classification: Ensure that all debt is correctly classified on the balance sheet between current and long-term portions. This depends on the payment schedule within the next 12 months and is a common area for misstatement.

- Analyze Refinancing Activities: If any debt was refinanced, extinguished, or modified during the period, verify that the accounting treatment, including the handling of any fees or gain/loss on extinguishment, complies with accounting standards.

By diligently verifying debt and interest expenses, you ensure accurate financial reporting and demonstrate robust control over your organization's financial obligations, which is a cornerstone of a successful audit.

7-Point Financial Audit Checklist Comparison

| Audit Procedure | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Review and Test Internal Controls | High - requires experienced judgment and specialized IT audit skills | High - time-intensive and resource-heavy | Identification of control weaknesses, reduced substantive testing, compliance assurance | Companies seeking operational improvements and regulatory compliance | Early detection of risks, valuable management insights |

| Cash and Bank Reconciliation Verification | Moderate - coordination with banks needed, follow-ups can be extensive | Moderate - straightforward testing but time-consuming if many accounts | Assurance over cash accuracy and fraud prevention, understanding liquidity | Entities with multiple bank accounts and high fraud risk | High regulatory focus, critical for cash flow accuracy |

| Revenue Recognition and Cutoff Testing | High - involves complex accounting standards and subjective judgments | High - extensive documentation review and specialized knowledge | Accurate revenue reporting, compliance with ASC 606/IFRS 15, prevention of misstatements | Revenue-heavy businesses with complex contracts | Addresses high inherent risk, critical for stakeholder decisions |

| Accounts Receivable and Allowance Analysis | Moderate - requires judgment and statistical techniques | Moderate - dependent on confirmations and subsequent collection testing | Evaluation of collectibility, allowance adequacy, and credit quality | Businesses with significant receivables and credit risk | Insights into customer relations and cash flow forecasting |

| Inventory Valuation and Physical Count Verification | High - physical counts and costing methods can be complex and disruptive | High - manpower and coordination needed for counts and testing | Accurate inventory valuation, detection of obsolescence, compliance with standards | Manufacturing, retail, and industries with large inventories | Strong physical evidence, directly impacts margins |

| Fixed Assets and Depreciation Analysis | Moderate - requires review of depreciation, impairment, and capital transactions | Moderate - testing calculations and asset verification | Proper asset capitalization, accurate depreciation, impairment assessment | Organizations with significant PP&E and capital expenditures | Systematic testing possible, physical verification of assets |

| Debt and Interest Expense Verification | Moderate - may require specialized review of complex instruments | Moderate - confirmations and legal document reviews needed | Accurate liability reporting, proper interest expense recognition, covenant compliance | Entities with significant borrowings and debt covenants | Easily confirmable balances, critical financial risk clarity |

Elevating Your Operations Beyond the Audit

Navigating the intricacies of a financial audit can feel like a monumental task, but as we've detailed, it's a process that can be systemized and mastered. The comprehensive financial audit checklist provided in this guide is more than a simple to-do list; it's a strategic framework for building institutional-grade operational integrity. From meticulously verifying cash and bank reconciliations to conducting thorough fixed asset and depreciation analyses, each step is a building block toward a stronger, more transparent financial foundation.

The true value of this process extends far beyond a clean audit opinion. For emerging fund managers, mastering this level of diligence is a critical differentiator. It demonstrates to potential and existing Limited Partners that your firm is not just focused on generating returns, but is also committed to robust governance, risk management, and operational excellence. This commitment is the bedrock of long-term trust and sustained capital allocation.

From Reactive Compliance to Proactive Excellence

The ultimate goal should be to transform the audit from a reactive, annual scramble into a proactive, continuous state of readiness. The key takeaways from our checklist reinforce this shift in mindset:

- Internal Controls are Foundational: Weak internal controls are often the root cause of audit issues. Regularly reviewing and testing these controls, as detailed in our first section, prevents minor discrepancies from escalating into material misstatements.

- Accuracy is in the Details: Items like revenue recognition and cutoff testing are not just about compliance; they are about accurately reflecting your firm's performance. Precision in these areas ensures that your financial statements tell the true story of your value creation.

- Documentation is Your Defense: Throughout the verification of accounts receivable, inventory, and debt, a clear, organized, and complete documentation trail is your best asset. This not only streamlines the audit process but also provides a concrete record of your firm's financial decisions and health.

By internalizing these principles, your back office evolves from a cost center into a strategic asset. The discipline required to maintain an audit-ready state fosters a culture of accuracy and accountability that permeates the entire organization, from the deal team to investor relations.

The Strategic Value of an Audit-Ready Operation

An audit is a snapshot in time, but the processes you build to prepare for it create lasting value. Diligently applying this financial audit checklist ensures that your firm is not just passing an examination but is building a resilient operational infrastructure. This infrastructure supports scalability, reduces operational risk, and frees up your team's most valuable resource: time.

Instead of dedicating weeks or months to manually gathering data, reconciling spreadsheets, and answering auditor queries, your team can focus on higher-value activities like performance analysis, LP communication, and sourcing the next great investment. This operational efficiency is not a luxury; for funds managing between $10M and $100M, it's a competitive necessity for scaling AUM and attracting institutional capital. The message to the market becomes clear: your firm is built on a foundation of integrity, ready for scrutiny, and poised for growth.

Ready to move beyond manual spreadsheets and embed audit-readiness into your daily operations? See how Fundpilot centralizes your data, automates fund administration, and provides a complete compliance trail, turning your next audit into a simple verification process. Explore the platform built for institutional-grade fund management at Fundpilot.