A Guide to Private Equity Limited Partners

Explore the world of private equity limited partners. This guide explains who LPs are, how they invest, and the strategies shaping today's market.

In the world of private equity, the fund managers—or General Partners (GPs)—often get the spotlight. But behind every successful fund is a group of crucial, yet often unseen, investors: the private equity limited partners (LPs).

These LPs are the financial backbone of the entire operation. They are institutions like pension funds, university endowments, and family offices, as well as high-net-worth individuals, who commit the capital that fuels the fund's investments.

The Role of Limited Partners in Private Equity

Think of a private equity fund as a complex voyage to find and grow valuable companies. The General Partner (GP) is the ship’s captain—charting the course, managing the crew, and making all the tough navigational decisions. The private equity limited partners are the financiers who fund the entire expedition, providing the resources needed to build the ship and supply the journey.

Without their capital, the ship never leaves the harbor.

This is the fundamental dynamic of private equity. LPs commit a specific amount of money to the fund but deliberately take a hands-off, passive role. This is where the "limited" part of their name comes from—their financial liability is strictly limited to the amount they've invested, protecting their personal assets from any losses beyond that commitment.

The Foundation of the LP-GP Relationship

The partnership between LPs and GPs is a classic case of symbiotic expertise. LPs bring the deep pools of capital required for large-scale investments, while GPs provide the specialized, on-the-ground knowledge needed to source deals, perform due diligence, and actively manage portfolio companies.

This structure is a win-win. It gives investors access to a sophisticated asset class without requiring them to become full-time dealmakers themselves. The entire relationship is formalized in a legally binding contract, which you can learn more about in our guide to the LP partnership agreement.

At its core, the LP role is one of strategic allocation and trust. They select expert managers (GPs) to navigate markets they cannot access alone, expecting premium returns for the long-term, illiquid nature of their commitment.

This passive investment model is what makes private equity tick. It’s a major component of the broader alternative investment landscape. By entrusting their capital to skilled managers, LPs act as the powerful, silent engine driving the entire industry—fueling buyouts, funding innovation, and spurring economic growth.

Who Are the Major Private Equity LPs

When we talk about private equity limited partners, it's easy to picture a single type of investor. The reality is far more interesting. The LP landscape is a collection of financial heavyweights, each with its own mission, timeline, and reason for investing.

These aren't just faceless pools of cash; they are strategic institutions tasked with growing and protecting massive amounts of capital. Their core job is to generate returns that can fund pensions for decades, finance university research, or preserve a nation's wealth for generations to come. This long-term focus is precisely what makes private equity so attractive to them.

The Institutional Powerhouses

The biggest LPs are typically the giants of the financial world—institutions that manage money for millions of people or entire countries. Their investment horizons are measured in decades, not quarters, making them a perfect match for the long-term nature of private equity.

- Pension Funds: Think of the organizations managing retirement savings for teachers, firefighters, and corporate employees. They have a non-negotiable need for steady, long-term growth to cover their future payouts, and private equity offers the potential for the kind of returns that help them get there.

- Sovereign Wealth Funds (SWFs): These are state-owned investment funds, created to invest government revenues for the long haul. With their enormous scale, they can write huge checks and commit to the best private equity funds for years, diversifying their national economies in the process.

- University Endowments: An endowment's goal is to support a university forever. The returns generated from their private equity investments can fund everything from student scholarships and new research facilities to faculty salaries, year after year.

These institutional LPs are the true titans of the investment world. An allocation from one of them doesn't just bring in capital; it's a powerful stamp of approval that signals a GP's credibility to the entire market.

Beyond these giants, family offices and high-net-worth individuals are also a crucial part of the LP community. Their focus is often on multigenerational wealth preservation, and they value private equity's ability to deliver strong returns that aren't always tied to the public markets' daily swings.

The Global Leaders in Private Equity Allocation

The amount of capital the top private equity limited partners control is simply staggering. A relatively small group of global institutions really sets the pace, with sovereign wealth funds from Singapore and the Middle East, along with major Canadian pension plans, consistently leading the pack.

This table showcases some of the world's largest institutional investors and their significant capital allocations to private equity, highlighting their influence on the market.

Top Global Private Equity Limited Partners by Allocation

| Limited Partner (LP) | Country | Private Equity Allocation (USD) | PE Allocation as % of Portfolio |

|---|---|---|---|

| Temasek Holdings | Singapore | $148 Billion | 53% |

| GIC Private Limited | Singapore | $144 Billion | 19% |

| CPP Investments | Canada | $137 Billion | 31% |

| Mubadala Investment Company | UAE | $125 Billion | 44% |

| Abu Dhabi Investment Authority (ADIA) | UAE | $120 Billion | 13% |

To give you a sense of the scale, Singapore’s Temasek Holdings leads the world with a $148 billion allocation to private equity, which accounts for more than half of its entire portfolio. Hot on its heels are GIC, also from Singapore, with $144 billion, and Canada's CPP Investments with $137 billion.

Major players like Mubadala Investment Company and the Abu Dhabi Investment Authority from the UAE both have allocations north of $100 billion. Their continued commitment underscores just how central private equity has become to the strategies of the world's most sophisticated investors. You can dive deeper into the numbers with the Private Equity International Global Investor Ranking.

How LPs Invest in Private Equity Funds

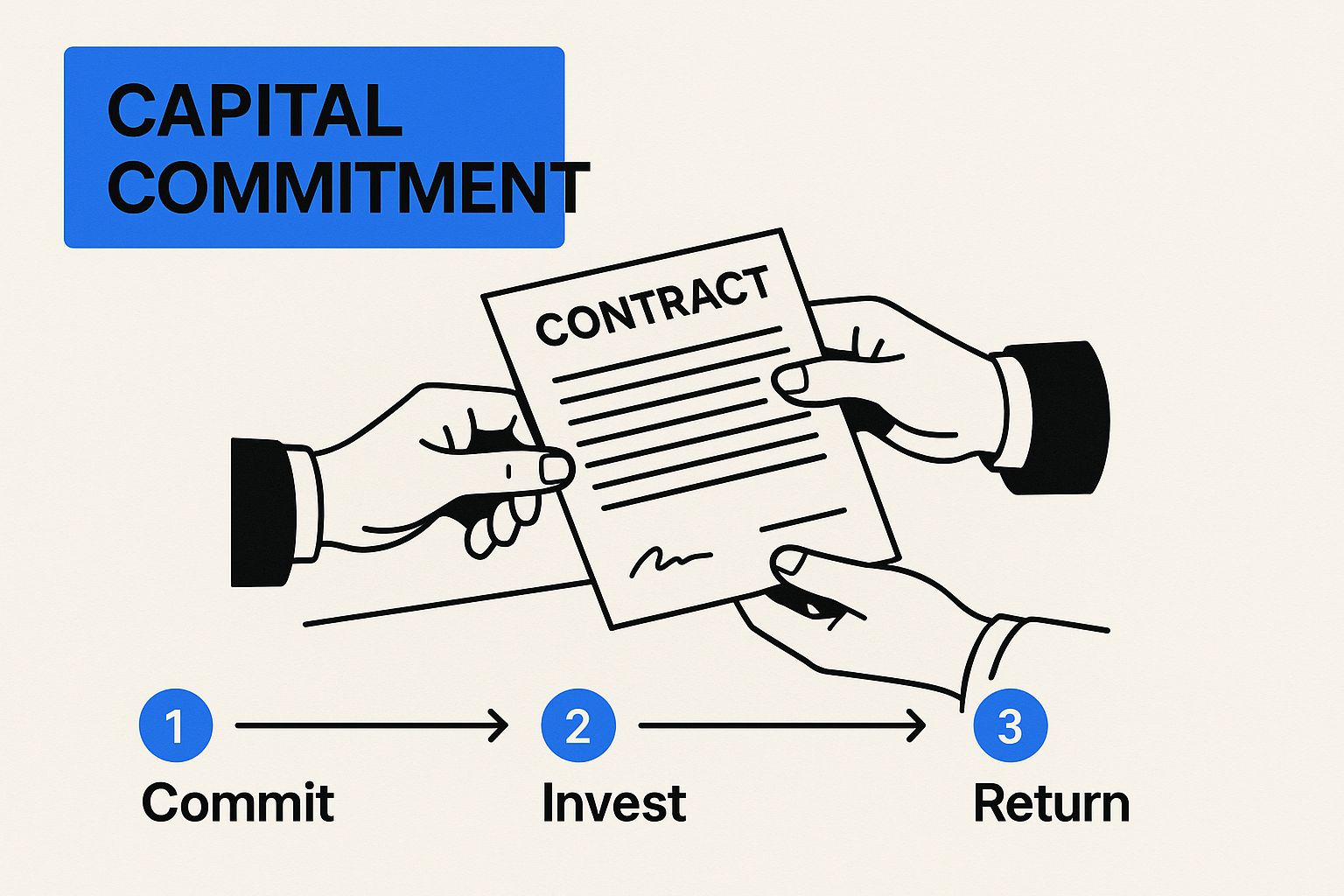

Investing in a private equity fund is nothing like buying a stock on the open market. A private equity limited partner doesn’t just wire over a lump sum and call it a day. Instead, they make a long-term capital commitment to a fund, which is typically structured to last for a 10-year lifecycle.

The process kicks off when a Limited Partner signs a formal agreement, pledging a specific amount—let's say $50 million—to the General Partner's (GP's) fund. But here's the key difference: that money stays in the LP's hands until the GP finds an investment and actually needs the cash. This "on-demand" funding structure is what makes the private equity model so efficient.

The infographic below shows this critical first step, where the legal and financial groundwork for the entire partnership is established.

Once that agreement is signed, a potential investor officially becomes a committed Limited Partner, and their journey with the fund begins.

The Capital Call Process

So, what happens when the GP finds a promising company to acquire? They initiate what's known as a capital call.

A great way to think about it is like a general contractor building a skyscraper. The contractor doesn't demand the entire project budget before breaking ground. Instead, they request funds in stages—first for the foundation, then for the steel frame, and so on.

A GP does the exact same thing. They "call" for a percentage of the LP's total commitment to finance a specific deal. For instance, on that $50 million commitment, the GP might issue a capital call for 10%, meaning the LP needs to provide $5 million to close the investment. This cycle repeats for each new acquisition the fund makes. If you want to dive deeper, you can explore our complete guide to capital calls in private equity.

This staged approach is a huge benefit for LPs. It lets them keep their capital invested and working elsewhere until the moment it's truly needed, which helps maximize their overall financial performance.

Understanding the J-Curve Effect

One of the most important, and often misunderstood, concepts for any private equity limited partner to grasp is the J-Curve. In the first few years of a fund's life, its performance is almost always negative. Why? Because the fund is busy paying management fees and transaction costs long before its new portfolio companies have had time to grow and generate real value.

The fund's net asset value (NAV) dips before it starts to climb, creating a performance graph shaped like the letter "J."

The J-Curve is a test of patience. It reflects the upfront costs of building a high-growth portfolio. Sophisticated LPs understand this initial dip is a normal and expected part of the private equity lifecycle, not a sign of poor performance.

As the years go by, the GP works to improve the portfolio companies. Eventually, they begin to sell them for a profit—a process known as an "exit"—and the fund's value starts to climb steeply. The cash generated from these exits is then sent back to the LPs in the form of distributions.

The ultimate goal, over that 10-year fund life, is for these distributions to massively outperform the initial capital invested, rewarding the LPs for their patient, long-term commitment.

How LPs Choose Which GPs to Back

Committing hundreds of millions—or even billions—of dollars to a General Partner (GP) is one of the highest-stakes decisions a private equity limited partner can make. This isn't just an investment; it's a partnership that can last a decade or more.

Think of it like an elite sports team hiring a new head coach. A winning record is non-negotiable, but you also need to believe in their strategy, their team culture, and their vision for future championships.

LPs put potential GPs through a grueling due diligence process, leaving no stone unturned. They aren't just looking for a fund with a flashy track record. They're searching for a partner with a repeatable, proven process for delivering top-quartile performance, fund after fund, no matter what the market is doing.

Evaluating the Track Record and Team

First things first: performance history. This is the initial hurdle where many GPs fall. LPs will pore over every detail of past funds, digging into metrics like Internal Rate of Return (IRR) and Distributions to Paid-in Capital (DPI). They need to see a consistent ability to not just generate paper gains, but to return cold, hard cash to investors.

But a great track record isn't the whole story. The team behind the numbers is just as important. LPs will dig deep, asking tough questions:

- Team Stability: How long has the core team been working together? Constant turnover is a huge red flag that often points to internal dysfunction.

- Succession Planning: What happens when the founders retire? LPs need to know the firm's magic isn't tied to one or two people.

- Relevant Experience: Does the team have true, specialized expertise in their target sector? A generalist approach rarely cuts it in private equity.

This whole process is designed to eliminate surprises down the road. To bring some structure to this intense evaluation, many institutions use standardized frameworks like those found in our guide to the ILPA Due Diligence Questionnaire.

Aligning Interests and Strategy

If the team and track record check out, the conversation shifts to alignment and strategy. An LP needs to be absolutely certain the GP’s interests are locked in step with their own.

The single most powerful way a GP can show they believe in their own strategy is the GP commitment. This is the amount of their own personal capital they invest in the fund. A meaningful commitment, typically 1-5% of the fund's total size, proves they have real skin in the game.

Beyond that personal investment, LPs scrutinize the fund’s proposed strategy. Is the investment thesis clear and compelling? Is the operational plan rigorous? LPs pay close attention to the GP's entire investment playbook, including their specific venture capital due diligence process.

Finally, it all comes down to the legal nuts and bolts in the Limited Partnership Agreement (LPA). This is where everything from management fees and carried interest to governance rights is hammered out. This negotiation ensures the terms are fair and the LP's capital is protected, setting the foundation for a successful partnership.

What LPs are Looking for Today: The Big Picture

The private equity world doesn't stand still, and neither do the strategies of the savviest private equity limited partners. We're seeing a real shift away from the old playbooks. Today’s investors are much more hands-on, using data to build their portfolios and demanding more control over where their capital goes.

It all boils down to two things: transparency and performance. LPs aren't just impressed by big numbers on a page anymore; they want to see actual cash coming back to them. This intense focus on liquidity is changing everything, from how they pick fund managers to how they structure their investments for the long haul.

It's All About the DPI Now

For a long time, the Internal Rate of Return (IRR) was the metric everyone talked about. Now, a different three-letter acronym is stealing the spotlight: DPI (Distributions to Paid-In Capital).

You can think of DPI as the ultimate "show me the money" metric. It cuts through the noise and answers one simple, crucial question: "For every dollar I've given you, how much cold, hard cash have you actually sent back to me?"

This focus on real cash-on-cash returns is a direct result of a market where paper valuations can feel a bit... abstract. LPs are making it crystal clear: they want to partner with GPs who can consistently turn investments into actual liquidity. A strong DPI proves a manager can see the whole process through—not just buying and building great companies, but successfully selling them and delivering the profits.

A high DPI is the gold standard for LPs. It represents real, realized value, not just a theoretical number on a spreadsheet. It’s the difference between being told your investment is worth a fortune and actually having the cash in your bank account.

Moving Away from Mega-Funds and Toward Specialists

We're also seeing a noticeable shift in sentiment toward the mega-funds. While these massive funds have scale, they're also under incredible pressure to put billions of dollars to work, which can make it tough to be nimble and find truly exceptional deals.

As a result, many LPs are turning their attention to smaller, more specialized funds—the ones that are laser-focused on a specific niche or industry. These specialist managers often bring a deeper level of operational expertise to the table, allowing them to spot opportunities the giants might miss.

Recent data backs this up. The Global Private Capital Barometer found that over a third of LPs expect new, independent manager spin-outs to outpace industry consolidation. That’s a clear signal of a growing appetite for fresh strategies. You can dive deeper into the findings of the Global Private Capital Barometer for more detail.

Getting More Hands-On with Co-Investments and Secondaries

LPs aren't just sitting back and waiting anymore; they're using more dynamic tools to actively manage their portfolios. Two strategies, in particular, have become incredibly popular:

-

Co-Investments: This is where an LP invests directly into a portfolio company right alongside the GP, often with lower (or no) fees. It’s a great way for them to get more skin in the game and double down on deals they truly believe in.

-

Secondaries: The secondary market is a game-changer. It allows LPs to buy and sell their stakes in existing funds. This provides a massive dose of liquidity and gives investors the flexibility to rebalance their portfolios in a way that just wasn't possible before.

Navigating the Challenges of a Complex Market

Let's be honest: today's market is a real paradox for private equity limited partners. On one hand, fundraising has become a much heavier lift. Capital isn't flowing as freely as it used to, the competition between General Partners (GPs) is intense, and getting a spot in a top-quartile fund takes more than just a check—it takes real conviction.

But here’s the flip side. This very scarcity has created something of a buyer's market. With GPs hungry for capital, smart LPs are finding themselves in a much stronger negotiating position. Suddenly, they have the leverage to ask for better terms, like lower management fees or more attractive co-investment rights. It’s a classic case of turning a challenging climate into a tangible advantage.

The Silver Lining: A Surge in Distributions

One of the biggest tailwinds for LPs right now is the recent and very welcome surge in liquidity. For the first time in what feels like forever, cash distributions from funds are actually outpacing capital calls. This means real, hard cash is flowing back into investors' pockets.

This isn't just a simple cash infusion; it's fundamentally shifting how LPs evaluate performance. While global private equity fundraising has slowed, this wave of distributions has hit one of the highest levels on record. This reversal is a game-changer for LPs, who are now laser-focused on Distributions to Paid-in Capital (DPI) as the ultimate measure of success. In fact, 2.5 times more LPs now rank DPI as their most important metric compared to just three years ago. You can dig deeper into this trend in McKinsey's global report.

How to Capitalize on the Current Market

In an environment like this, the most sophisticated LPs aren't just waiting it out. They're actively adapting their playbooks to make the most of these unique conditions. It all comes down to being more selective and data-driven than ever before.

Here’s what that looks like in practice:

- Backing the Proven Winners: LPs are doubling down on GPs who have a clear, demonstrable track record of returning capital, not just on paper but in actual cash, through all kinds of market cycles.

- Negotiating From a Position of Strength: They're using their newfound leverage to secure more favorable fund structures and better economic terms that directly benefit their bottom line.

- Building All-Weather Portfolios: The focus has shifted toward creating more resilient portfolios. This means diversifying across different strategies and using tools like secondaries and co-investments to construct portfolios built to perform well into the future, no matter what the market throws at them.

Common Questions About Private Equity LPs

Diving into the world of private equity can feel a bit like learning a new language. Let's clear up some of the most common questions people have, especially when it comes to the investors who power these funds.

What's the Real Difference Between an LP and a GP?

Think of it like building a house. The Limited Partner (LP) is the person who funds the project—they provide the capital and trust the experts to get the job done. Their financial risk is capped at whatever amount they put in.

The General Partner (GP), on the other hand, is the master builder and architect. They find the land (the investment), manage the construction (grow the company), and handle the sale. They are in the trenches every day, which means they also carry unlimited liability for the project's outcome.

How Do LPs Actually Make Money?

It's a straightforward, if not simple, process. LPs see a return on their investment only when the fund's portfolio companies are sold for a profit.

Here’s the breakdown:

- Growing the Business: The GP spends years actively working with the companies in the fund, aiming to dramatically increase their value.

- Cashing Out: Eventually, the GP finds the right time to sell a company, whether through a sale to another firm or by taking it public in an IPO.

- Sharing the Profits: The money from that successful "exit" is then paid out to the private equity limited partners.

The whole point for an LP is to earn a return that beats what they could get in the public stock market. That premium is their reward for tying up their capital for years and taking on more risk.

It's a classic partnership: LPs provide the fuel (capital), and GPs drive the vehicle (the fund). The GP handles all the bumps and turns along the way, but the LP gets their share of the prize when they reach a profitable destination.

Can an Average Person Be a Limited Partner?

Technically, yes, but it’s a very exclusive club. This role is typically reserved for “accredited investors” or “qualified purchasers.” These are regulatory terms for individuals who meet high-income or high-net-worth requirements, proving they can handle the financial risk.

Even for those who qualify, the price of entry is steep—minimum commitments often start at $1 million or more. For most people, a more accessible route is to invest in publicly traded private equity firms or specialized "funds of funds" that bundle smaller investments.

Managing these crucial LP relationships and delivering top-tier reporting is what sets successful funds apart. Fundpilot gives emerging managers the platform they need to automate fund administration, keep LPs informed, and present performance data like a seasoned pro. Upgrade your LP reporting with Fundpilot today.