A Guide to Capital Call in Private Equity

Understand the capital call in private equity with our complete guide. Learn the process, timelines, and legal duties for both GPs and LPs.

When you hear the term capital call, think of it as a private equity fund manager making a "cash-in" request to their investors. The manager, known as the General Partner (GP), formally asks the investors, or Limited Partners (LPs), to send in a portion of the money they've already promised to the fund. This "just-in-time" approach means money is only collected and put to work when a real investment opportunity is on the table, preventing large sums from sitting around gathering dust.

What Exactly Is a Capital Call in Private Equity?

Let's break it down with an analogy. Imagine a private equity fund is like building a custom home. The GP is the general contractor, and the LPs are the homeowners funding the project. The contractor doesn't ask for the entire cost of the house upfront. Instead, they request funds in stages—when it's time to pour the foundation, then again for the framing, and later for the roofing. A capital call in private equity works the exact same way.

This process, also called a drawdown, is fundamental to how private equity works. It lets GPs call on a fraction of an LP's total committed capital right when they need it. The funds might be for a new company acquisition, to cover operational fees for the fund, or to inject more cash into an existing portfolio company. This efficiency is a massive advantage over other investment models that demand all the money on day one.

The Roles of GPs and LPs

The dynamic between the General Partner and the Limited Partners isn't based on a handshake; it's all laid out in a critical legal document: the Limited Partnership Agreement (LPA). This agreement is the rulebook that governs every single capital call.

- General Partners (GPs) are the deal-makers and fund managers. Their job is to hunt for promising investments, perform rigorous due diligence, and run the fund's day-to-day operations. When they find a deal, they're the ones who send out the formal capital call notice.

- Limited Partners (LPs) are the investors supplying the fuel for the fund. Once they receive a capital call, their main responsibility is to wire the requested funds within the agreed-upon deadline, which is usually around 10 to 15 business days.

The whole point of this staged funding is to boost a fund's Internal Rate of Return (IRR). By making sure cash isn't sitting idle—a problem known as "cash drag"—GPs can post much stronger performance numbers for their investors.

The capital call process unfolds in a few distinct steps. Here’s a quick overview of what that looks like from start to finish.

Key Stages of a Capital Call

| Stage | Description |

|---|---|

| 1. Investment Opportunity Identified | The GP finds a compelling investment, completes due diligence, and decides to move forward with the acquisition or funding. |

| 2. Capital Call Notice Issued | A formal notice is sent to all LPs, detailing the amount due from each, the total call amount, the purpose, and the deadline. |

| 3. LPs Fulfill the Call | LPs wire their pro-rata share of the required capital to the fund's designated bank account by the specified date. |

| 4. Funds are Deployed | Once the capital is collected, the GP uses it to complete the investment, pay expenses, or fund other specified needs. |

As you can see, it's a structured and predictable sequence of events designed for efficiency and clarity.

Why This Model Works

So, why go through all this trouble? The capital call structure is a cornerstone of private equity because it works beautifully for both sides. For GPs, it guarantees that when they find a great deal, the money is ready to go without delay.

For LPs, it provides a ton of financial flexibility. They don't have to write a massive check on day one. Instead, they can keep their capital working elsewhere, managing their liquidity much more effectively until the funds are actually needed. It's a symbiotic relationship that turns commitments into active investments with precision, right when opportunity strikes.

The Capital Call Process Step by Step

A capital call isn't just a one-off request for money. It's a carefully choreographed process that turns a paper commitment into actual cash the fund can put to work. Think of it as a well-oiled machine designed to keep things clear and efficient for everyone involved, from the General Partners (GPs) managing the fund to the Limited Partners (LPs) who've invested in it.

The whole thing kicks off when the GP spots an opportunity or a need. This could be anything from pouncing on a deal to acquire a promising new company, to making a vital follow-on investment in a business already in their portfolio. Sometimes, it's just to cover the fund's own management fees and operational costs. Whatever the reason, once the amount is finalized, the formal process begins.

Initiating the Call and Notifying Investors

The first real step is to create the capital call notice. This is much more than a simple email asking for cash; it's a formal, legally binding document. Its main purpose is to give LPs all the details they need to wire the funds with complete confidence.

Every notice worth its salt will contain a few critical pieces of information:

- Total Call Amount: The full amount the fund is pulling from all its investors combined.

- Individual LP Share: The specific slice of that total that each LP is responsible for, calculated pro-rata based on their commitment.

- Purpose of the Call: A straightforward explanation for why the money is needed (for example, "to fund the acquisition of Company XYZ").

- Due Date: The hard deadline for when the funds need to hit the bank, which is usually 10 to 15 business days out.

- Wiring Instructions: The exact bank account details for the transfer.

Once drafted, this notice is sent out securely to every LP, which officially starts the countdown.

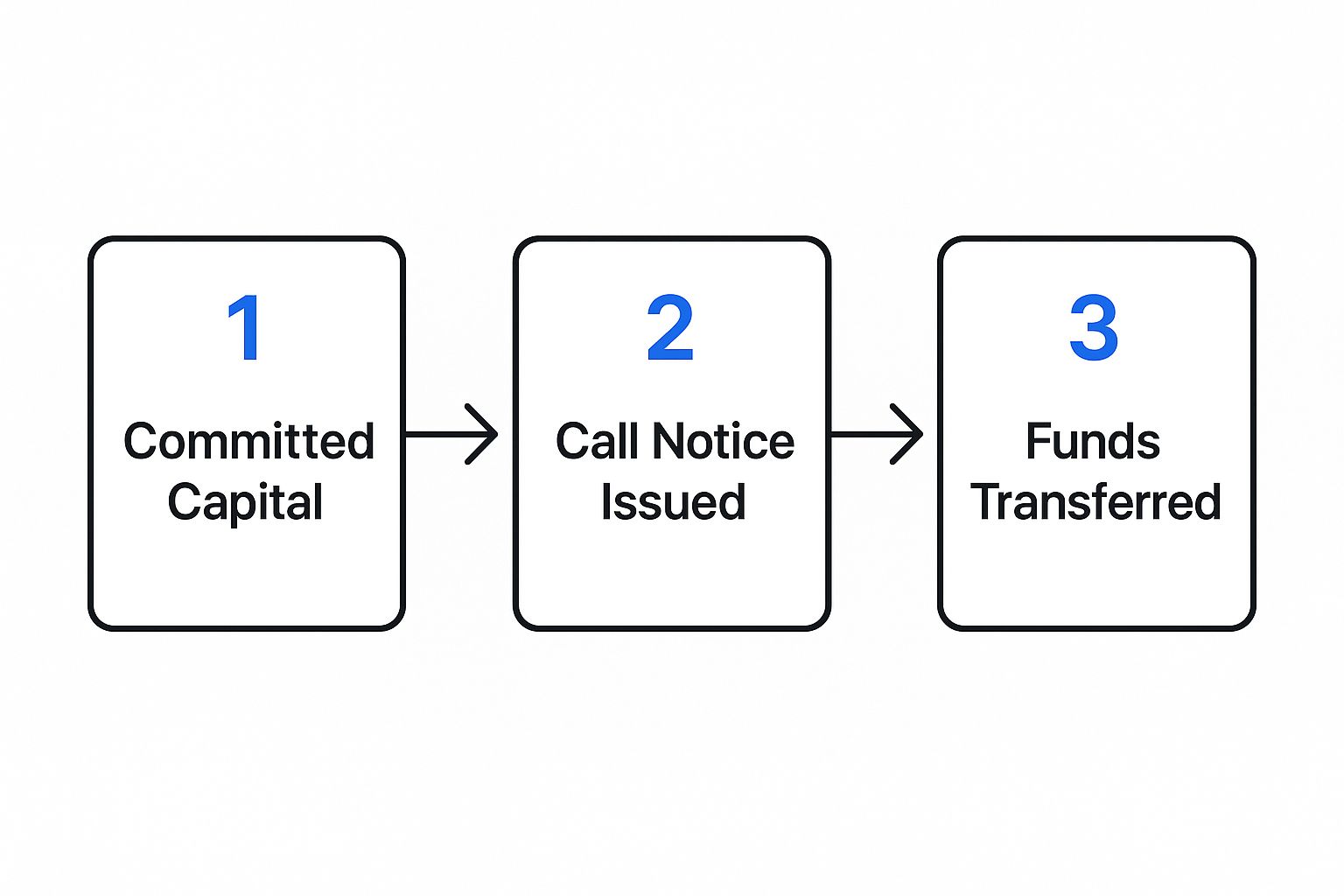

This image lays out the simple, linear journey of a typical capital call.

As you can see, it’s a three-stage flow, starting with the LP's initial commitment and ending with the cash transfer when the GP makes the call.

The LP Response and Fund Confirmation

After getting the notice, the ball is in the LP's court. Their team will do a quick but thorough check. They'll confirm the amount is correct based on their pro-rata share and double-check that the reason for the call lines up with the fund's investment strategy as laid out in the Limited Partnership Agreement (LPA).

For LPs, this verification step is crucial. It’s about ensuring every drawdown is contractually sound and transparent, maintaining trust in the GP's management and operational integrity.

Once everything checks out, the LP gets their bank to wire the money over to the fund's account, making sure it arrives before the deadline.

The final piece of the puzzle belongs to the GP. As the wires start coming in, the fund's back-office team is busy tracking each payment. They reconcile every dollar received against what was requested in the notice. After confirming the funds have landed, they'll send a confirmation of receipt back to the LP, officially closing the loop on that capital call. The capital is now ready to be deployed.

Decoding Capital Call Timelines and Notices

When a capital call notice lands on your desk, two things jump out immediately: time and information. The timeline for a capital call in private equity isn’t just pulled out of a hat. It's a carefully structured period meant to give Limited Partners (LPs) enough breathing room to get their funds in order without kicking off a frantic scramble.

This whole process is dictated by the fund's official playbook, the Limited Partnership Agreement (LPA).

Typically, you can expect a notice period of 10 to 15 business days to send the money. This window is a critical feature of the agreement, not just a polite gesture. It’s designed to give investors like you time to manage your own liquidity, shift assets if needed, and set up the wire transfer in an orderly way. The goal is to avoid the pressure cooker of a last-minute cash demand.

Ultimately, this structured timing is all about keeping the relationship between the General Partner (GP) and their investors healthy. It makes the entire funding process predictable and professional.

Anatomy of a Capital Call Notice

Think of the capital call notice itself as an itemized invoice for your investment. It’s a straightforward document that lays out exactly what the GP is asking for and why. Before a single dollar leaves your account, it's smart to give this document a thorough review to make sure it's accurate and lines up with the LPA.

A standard notice will always break down a few key details:

- Total Drawdown Amount: This is the total amount of capital the GP is collecting from all LPs in this particular call.

- Your Pro-Rata Share: Here’s your specific piece of the pie—the exact amount you need to contribute, calculated from your total commitment to the fund.

- Due Date: The hard deadline. Your funds absolutely must be in the fund's bank account by this date.

- Purpose of the Call: A clear explanation of where the money is going, like "to fund the acquisition of Company X."

Understanding and verifying each element of the notice is a fundamental part of an LP's due diligence. It confirms the GP is operating within the agreed-upon terms and provides a transparent view of how your capital is being put to work.

The notice will also include the specific wiring instructions you'll need for the transfer. It’s always a good idea to double-check these details to avoid any simple, but costly, transactional errors. By taking the time to dissect each notice, LPs can fulfill their commitment with confidence, knowing every call is justified, accurate, and ready for a smooth transfer.

The Legal Framework That Governs Capital Calls

A capital call isn't just a friendly request for cash. It’s a formal demand, and its power comes from a critical legal document: the Limited Partnership Agreement (LPA).

Think of the LPA as the fund's constitution. It’s the rulebook that spells out every detail of the relationship between the General Partner (GP) and the Limited Partners (LPs). This document lays down the law for everything, creating a predictable and enforceable framework that everyone has to follow.

From the required notice period—usually 10 to 15 business days—to the specific formula for calculating each LP's contribution, the LPA dictates the entire process. It's the single source of truth that keeps GPs in line and ensures LPs know exactly what's expected of them. When you sign it, you're entering a legally binding commitment.

Fiduciary Duty and Investor Protections

At the core of this whole relationship is a concept called fiduciary duty. This isn't just a buzzword; it's a serious legal obligation. It means the GP must act purely in the best financial interests of their investors.

So, when a GP issues a capital call, they can't just do it on a whim. They need a legitimate, strategy-driven reason, whether it’s for a fantastic investment opportunity they've lined up or to cover necessary fund expenses. This duty is a crucial protection for LPs, giving them confidence that their money isn't being called down frivolously or used recklessly. You can explore more about the legal intricacies governing fund management in our detailed overview.

When an LP Defaults on a Capital Call

It doesn't happen often, but when an LP fails to send in their money, it's a major problem. This is a serious breach of the LPA, and the consequences are severe. The agreement gives the GP some powerful tools to protect the fund and the other investors from the cash shortfall.

The penalties are designed to be painful. They can include:

- Steep Interest Penalties: The GP can start charging high interest on the amount owed.

- Loss of Future Profits: The defaulting LP might be cut out of any profits from new investments.

- Forfeiture of Stake: In the most serious cases, the GP can actually force the LP to give up their entire investment in the fund.

These measures aren't just for show. They highlight just how serious a capital commitment is. The entire private equity model relies on the certainty that when a GP finds a great, time-sensitive deal, the promised money will be there.

The pressure to meet these calls can be immense, particularly when the economy gets rocky. We saw this play out during the 2008 financial crisis. While capital calls held steady at first, they plummeted by 50% in 2009 as new deals simply vanished. It’s a stark reminder of how much the broader economy can influence the rhythm of a fund.

A capital call in private equity never happens in a vacuum. It’s deeply tied to the ebb and flow of the wider economy. Think of the economic climate as the weather forecast for a fund’s investment strategy—it determines whether it’s a good day to build something new (make an acquisition) or time to batten down the hatches (support existing portfolio companies).

General Partners (GPs) are constantly reading the macroeconomic tea leaves to decide when to call capital and what to use it for. A fund's game plan has to be flexible, shifting with the market. This means the timing and reason behind every capital call are a direct reflection of what's happening in the financial world.

Interest Rates and Market Confidence Can Change Everything

When interest rates are low and the market is humming, it’s go-time for deal-making. Cheap borrowing fuels a more aggressive hunt for leveraged buyouts and new acquisitions. This environment often triggers a higher frequency of capital calls because GPs need to move fast to close deals. During these boom times, LPs should brace for a quicker drawdown schedule.

But when interest rates start climbing and uncertainty creeps in, the whole strategy can flip on a dime. Deal flow might slow to a trickle as expensive debt makes new acquisitions look far less appealing. In this kind of climate, GPs shift from playing offense to playing defense.

When the economy gets rocky, the reason for a capital call often changes. Instead of funding shiny new deals, GPs might call capital to build a financial moat around their existing portfolio companies, helping them ride out the storm and come out stronger on the other side.

This defensive playbook means the capital is typically used for:

- Shore Up Balance Sheets: Injecting cash into portfolio companies to pay down debt or build up cash reserves.

- Fund Day-to-Day Operations: Covering temporary cash flow gaps when sales slow down or supply chains get messy.

- Strategic Bolt-On Acquisitions: Helping a strong portfolio company snap up a smaller, struggling competitor at a good price.

The financing environment is what really drives this cycle. Take what happened between 2022 and 2023, when global interest rates shot up. Private equity firms faced a steep rise in borrowing costs, which slammed the brakes on deal activity. But as conditions began to ease, new loan volumes for PE-backed borrowers nearly doubled, and capital calls started picking up again.

You can dive deeper into these trends by checking out the full global private markets report. Grasping this relationship is key for both GPs and LPs to anticipate the pace and purpose of capital calls throughout a fund's entire lifecycle.

Best Practices for Managing the Capital Call Process

When capital calls run smoothly, it’s a clear sign of a healthy, trusting partnership between a fund manager and their investors. It shows operational excellence. For both General Partners (GPs) and Limited Partners (LPs), getting this process right can transform a logistical headache into a seamless, predictable part of the investment cycle.

The key is to build strategies around transparency, communication, and efficiency. This isn’t just about moving money; it’s about strengthening relationships.

For General Partners: Communication is Everything

As a GP, your goal is to eliminate surprises and build unwavering confidence with every interaction. It’s all about clear communication and operational discipline.

- Give a Heads-Up: Before the formal notice ever goes out, give your LPs an informal heads-up about an upcoming capital need. This simple courtesy goes a long way, giving them time to prepare their liquidity.

- Establish a Rhythm: For predictable expenses like management fees, try to stick to a consistent schedule. A predictable cadence helps your LPs forecast their cash outflows and manage their own books much more effectively.

- Embrace Modern Tools: Ditch the spreadsheets. Modern fund administration software can automate everything from generating notices to tracking payments. It also gives LPs a secure portal to access their documents, which drastically cuts down on manual errors and boosts transparency. For more on this, you can find a ton of resources on our blog.

For Limited Partners: Stay Prepared

If you’re an LP, the name of the game is proactive liquidity management. Failing to meet a capital call is simply not an option in the world of private equity, so preparation is paramount.

One of the smartest things an LP can do is maintain a "liquidity sleeve." This is a dedicated portion of your portfolio held in low-risk, easily accessible assets, ready to be deployed for capital calls without forcing you to sell other investments at an inconvenient time.

It’s also crucial to keep a close eye on fund communications and broader economic shifts. For instance, the fundraising environment has been cautious lately. According to one report, global buyout fundraising fell by 23% in 2024, down to $401 billion.

Trends like this can directly impact how frequently and when a fund might call for capital. Staying informed makes your own financial planning that much sharper. You can dig deeper into the 2025 private equity outlook from Bain & Company for more on what’s ahead.

Common Questions About Private Equity Capital Calls

As we've unpacked the mechanics of a capital call in private equity, it’s natural for a few common questions to pop up. Let's tackle some of the most frequent ones from both General Partners (GPs) and Limited Partners (LPs) to clear up any lingering confusion.

The whole process hinges on a blend of legal agreements and good old-fashioned trust, but things can get tricky when theory meets reality. Getting a handle on these nuances is what separates a smooth investment cycle from a bumpy one.

Can an LP Refuse a Capital Call?

The short answer is no, not without serious repercussions. Backing out of a capital call is a major breach of the Limited Partnership Agreement (LPA), the legally binding contract that underpins the entire fund.

The penalties for defaulting are deliberately harsh. An LP could face steep financial fines, lose their right to any future profits, or even be forced to forfeit their entire investment in the fund. The private equity model relies on LPs honoring their commitments so GPs can close deals and run the fund effectively.

What Is the Difference Between Committed and Called Capital?

It’s easy to mix these two up, but they represent two very different points in the investment journey.

- Committed Capital: This is the total amount of money an LP has promised to invest in the fund over its entire lifespan. Think of it as their pledge, not cash that's been handed over.

- Called Capital: Also known as paid-in capital, this is the portion of the commitment that the GP has actually requested—or "called"—and received from the LP so far.

A simple analogy is to think of committed capital as your total credit card limit. Called capital is how much of that limit you've actually spent. The remaining, unspent amount is what the industry calls "dry powder," which is the capital the GP still has available to deploy for new investments.

Are There Data Privacy Concerns with Capital Calls?

Without a doubt. Capital call notices, subscription documents, and all the communication in between are packed with sensitive personal and financial data. GPs aren't just expected to protect this information; they are legally required to.

Keeping this data secure is fundamental to maintaining investor trust and steering clear of serious legal trouble. You can dive deeper into the essentials of data protection and compliance for funds to understand the best practices for handling investor information. Solid data governance isn't just a suggestion—it's the law.

Ready to move beyond spreadsheets and streamline your capital calls? Fundpilot offers an institutional-grade platform to automate fund administration, enhance LP communications, and maintain audit-ready records. Request a demo of Fundpilot today and see how we help emerging managers operate like top-tier firms.