Private Equity Value Creation Playbook

Unlock the strategies behind private equity value creation. Our expert playbook explains how top firms drive growth and maximize returns in portfolio companies.

Private equity value creation is all about what happens after the deal is signed. It’s the process where a PE firm actively works to make the company they just bought more profitable and perform better.

Think of a PE firm as an expert home renovator, but for businesses. They don't just buy a company to hold it; they buy it with a clear plan to fundamentally rebuild it from the inside out, all to increase its value for an eventual sale.

The Blueprint for Building Better Businesses

At its heart, modern private equity has evolved way beyond simple financial engineering. While cleaning up a company's balance sheet is still on the checklist, today's PE firms are more like strategic partners. They roll up their sleeves and get deeply involved in the day-to-day business.

The goal? To build a company that is stronger, more efficient, and ultimately more valuable than the one they started with. This hands-on approach isn't about financial smoke and mirrors; it's grounded in tangible, operational improvements. PE firms bring a deep bench of experience, powerful industry connections, and specialized knowledge that a company's management might not have on its own.

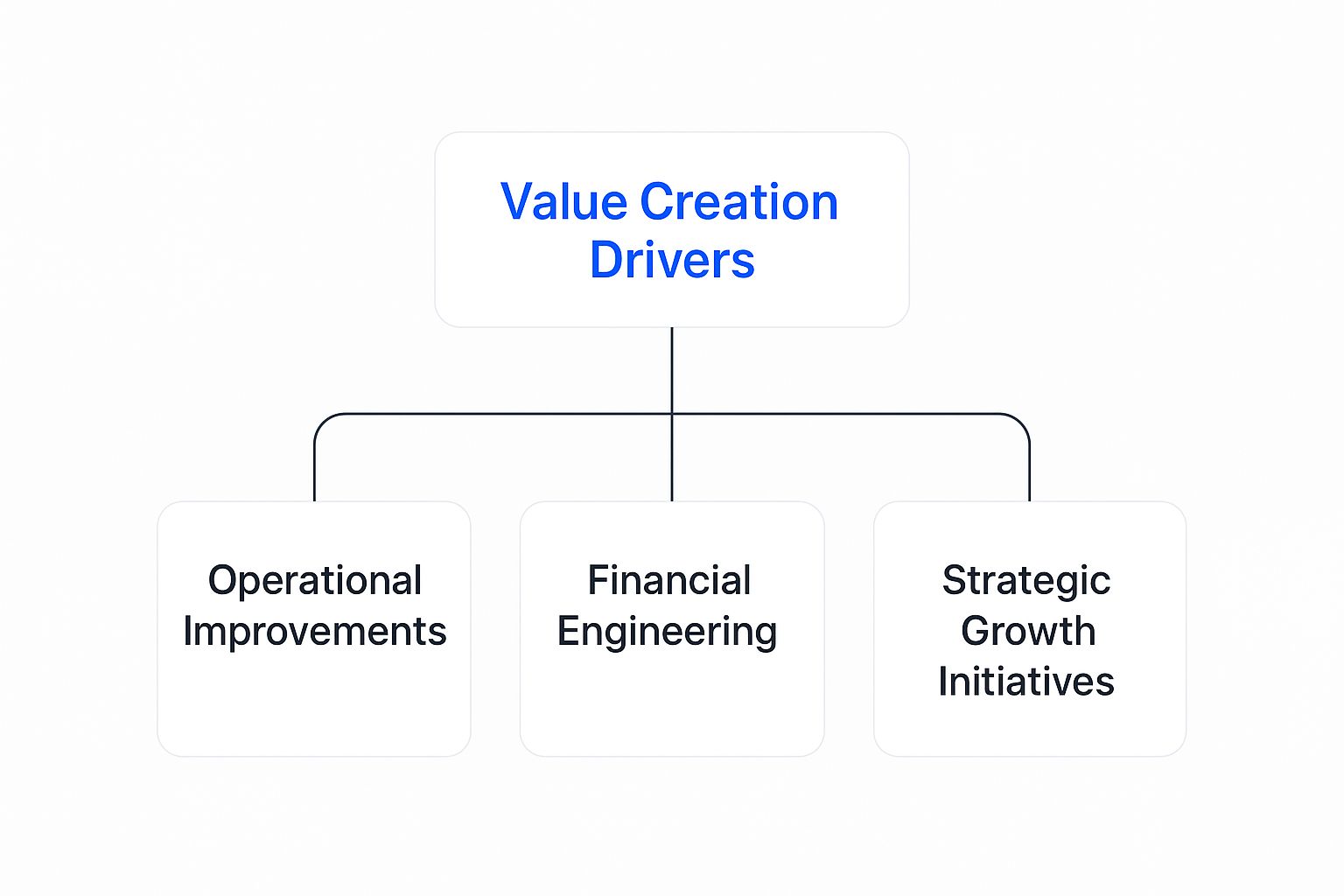

The Three Pillars of Value Creation

Every decision a PE firm makes during its ownership period is typically guided by three core objectives. These pillars form the foundation of their entire strategy:

- Revenue Growth: This is all about boosting the top line. It could mean pushing into new markets, launching new products, or completely overhauling sales and marketing.

- Margin Expansion: Here, the focus shifts to profitability. It’s about making the company more efficient by cutting unnecessary costs, streamlining operations, and getting smarter with pricing.

- Multiple Expansion: This is about making the company a more attractive asset, so the next buyer is willing to pay a premium for it. A higher valuation multiple is often the result of transforming the business model or solidifying its market leadership.

This diagram helps visualize how these different drivers work in concert.

As the graphic shows, real value creation isn’t a one-trick pony. It’s a sophisticated blend of financial, operational, and strategic initiatives that all have to work together to drive growth.

To put it simply, here’s how these pillars translate into action.

The Core Pillars of Private Equity Value Creation

| Value Creation Pillar | Objective | Typical Actions |

|---|---|---|

| Revenue Growth | Increase top-line sales and market share. | Entering new geographic markets, launching new product lines, optimizing pricing strategies, and investing in sales and marketing teams. |

| Margin Expansion | Improve the company's core profitability. | Streamlining supply chains, implementing lean manufacturing, automating processes, cutting overhead, and renegotiating vendor contracts. |

| Multiple Expansion | Increase the company's valuation at exit. | Improving governance, building a world-class management team, shifting to a recurring revenue model, and establishing a clear strategic advantage. |

These pillars provide the framework, but the execution is where the real work happens.

Where the Real Value Comes From

While all three pillars matter, the data clearly shows one has become the primary engine of PE returns in today's market.

A deep dive into more than 10,000 private equity deals revealed that revenue growth is the undisputed champion, accounting for about 54% of the value generated. Multiple expansion follows at 32%, with margin expansion contributing the final 14%.

This statistic highlights a massive shift in the industry. The old playbook of just slashing costs or riding a wave of rising market valuations is no longer a reliable path to success. The top-performing firms are the ones that can create genuine, sustainable top-line growth. You can dig into more of the data in this private equity value creation research to see the complete analysis.

By focusing on these areas, PE firms create a powerful flywheel. Growing revenue often improves margins as the business scales, and a company with both strong growth and healthy profits will naturally command a higher valuation multiple. This holistic approach is the essence of modern private equity value creation—and the secret to delivering standout returns for investors.

Mastering the Levers of Operational Value Creation

If strategy is the architect's blueprint, then operational levers are the power tools private equity pros use to actually build a better, stronger company. This is where the rubber meets the road—where theory gets turned into tangible results. Operating partners get in the trenches with management to fine-tune the company’s engine, making it run faster, smoother, and more profitably.

We’re not talking about vague, high-level goals here. These are specific, measurable actions. Think of an underperforming business like a gifted but messy mechanic's garage. All the right tools might be lying around, but they’re disorganized, dull, and nobody’s using them properly. The PE firm steps in as the master mechanic, systematically organizing the shop, sharpening the tools, and showing the team how to get the most out of them.

Building a Professional Sales Engine

One of the very first places we look for value is the sales function. It’s amazing how often a "gut-feel" or inconsistent sales process is the main thing holding a great company back from explosive growth. Turning that art into a science is a cornerstone of modern private equity value creation.

The first step is usually getting everyone onto a proper Customer Relationship Management (CRM) system like Salesforce or HubSpot. Moving from a chaotic mess of spreadsheets to a single source of truth for customer info, sales activity, and pipeline health is a game-changer. It’s the difference between trying to navigate with a crumpled, hand-drawn map and using a high-precision GPS.

Once the data is under control, the focus shifts to process and people. This typically involves:

- Standardizing the Playbook: Getting the whole team trained on a proven sales methodology, like consultative or solution selling. This ensures every potential customer gets a consistent, professional experience.

- Defining What Success Looks Like: Establishing clear Key Performance Indicators (KPIs) is critical. Metrics like lead conversion rates, average sales cycle length, and deal size tell you exactly what’s working and where to focus coaching efforts.

- Aligning Incentives with Goals: You get what you reward. We often redesign commission structures to push the team toward the right behaviors, whether that's landing higher-margin deals or bringing in valuable new customers.

Optimizing Pricing for Maximum Profit

So many companies, especially those that are still founder-led, are leaving a ton of money on the table with their pricing. PE firms bring a much more rigorous, data-driven approach to pricing strategy, which can boost revenue and margins without selling a single extra product. It’s often the fastest and most powerful lever you can pull.

I saw this firsthand at a portfolio company recently. A PE firm used generative AI to comb through years of transaction data, and it immediately flagged entire service lines that were seriously underpriced. A simple pricing adjustment based on that insight added $10 million in annual revenue with almost no extra cost.

The goal is to move beyond simple "cost-plus" thinking and get more strategic. Some of the most effective tactics include:

- Segmenting Your Customers: Figure out which customers are willing to pay a premium and what they value most. This lets you create tiered pricing that captures more value from each segment.

- Pricing Based on Value: Instead of just marking up your costs, tie your price directly to the tangible value and ROI you deliver to the customer.

- Using Dynamic Models: In some industries, you can implement systems that adjust prices based on real-time demand, competitor moves, or even the time of year.

This kind of granular work uncovers hidden profit pockets and makes sure the company is being paid what it's truly worth. It’s more like a surgical procedure than a sledgehammer.

Driving Efficiency with the Right Technology

Beyond sales and pricing, injecting the right technology into a company's core operations is a massive lever for efficiency. When you automate repetitive work and use data to make smarter decisions, you slash costs and free up your best people to focus on what really matters.

This could mean upgrading or implementing an Enterprise Resource Planning (ERP) system to get finance, HR, and the supply chain all speaking the same language. For a manufacturer, it might be installing IoT sensors on the factory floor to predict when a machine needs maintenance, cutting down on expensive downtime. For a professional services firm, it might be using AI to process documents, saving thousands of hours of manual labor.

The impact is huge. By finding the real operational bottlenecks and deploying the right tech, PE firms can build a much more scalable and resilient business. Each of these levers—sales, pricing, and technology—works together to fundamentally transform how a company operates, delivering the "operational alpha" that sets the best private equity deals apart.

The Buy-And-Build Growth Playbook

When it comes to private equity value creation, one of the most powerful and widely used strategies is the "buy-and-build." This isn't about patient, organic growth. It’s an aggressive, deliberate approach for rapidly scaling a business and transforming it into a market leader.

Think of it like building a powerful freight train from scratch. A private equity firm starts by finding a solid, well-run "platform" company—this is the engine. From there, they strategically acquire and "bolt on" smaller, complementary businesses. These "add-on" or "tuck-in" acquisitions are the railcars, each bringing something valuable to the train, like new services, customers, or access to different regions.

The result? A combined business that scales far faster than any of its competitors could on their own. This strategy is particularly effective in fragmented industries—think dental practices, HVAC services, or niche software providers—where countless small players exist but lack the capital or scale to truly dominate. By rolling them up, a PE firm can create an enterprise worth far more than the sum of its individual parts.

The Dual Engines of Value Creation

So where does the value actually come from? The buy-and-build playbook is driven by two key forces that work together: multiple arbitrage and operational synergies. It’s this one-two punch that accelerates growth, boosts profitability, and ultimately leads to a much higher sale price down the road.

First up is multiple arbitrage. In simple terms, bigger is better in the eyes of the market. A large, stable company pulling in $100 million in revenue will command a higher valuation multiple (say, 10x EBITDA) than a small local shop with $5 million in revenue (which might only fetch 5x EBITDA).

A PE firm exploits this by buying smaller companies at those lower multiples and integrating them into the larger platform. The earnings from those small acquisitions are instantly "re-rated" at the platform's higher valuation multiple. It’s a powerful financial lever that creates value from day one.

Unlocking Powerful Operational Synergies

While multiple arbitrage gives you a great head start, real, sustainable value is built through deep operational synergies. This is where the hard work of integration pays off, creating massive opportunities to streamline how the entire operation runs.

The real magic of a roll-up is imposing a single, professionalized operating model across a collection of previously independent businesses. You centralize expertise, get rid of redundant costs, and build a unified growth engine that none of the smaller companies could have created alone.

This integration process unlocks value in a few critical areas:

- Cost Synergies: The most obvious win is centralizing back-office functions. Instead of every small company having its own finance, HR, and IT teams, you consolidate them. This eliminates redundant roles and systems, slashing overhead. The combined company also gains immense purchasing power, allowing it to negotiate much better deals with suppliers.

- Revenue Synergies: A bigger, integrated business can generate sales that were impossible before. A classic move is to cross-sell products and services across the newly combined customer base. For example, if you acquire a company with a specialized service, you can immediately start offering it to the platform's much larger client roster, opening up brand-new revenue streams overnight.

A Practical Example of the Playbook

Let's walk through how this works in the real world. Imagine a PE firm buys a top-tier regional IT services provider in the Northeast. It’s a great business, but its growth is limited by geography. This is the platform.

Here's how the buy-and-build unfolds:

- Acquisition 1: They purchase a smaller IT firm in the Southeast. Instantly, the company has a national footprint.

- Acquisition 2: Next, they acquire a boutique cybersecurity firm. This adds a high-demand, high-margin service to their portfolio.

- Integration: Finally, they merge all three companies onto a single ERP and CRM system. They centralize billing and HR and retrain the entire sales team to sell the newly expanded suite of services.

Through this disciplined process, a regional player becomes a national powerhouse with a diverse, high-value service offering. The new entity is bigger, more efficient, and far more profitable, making it a highly attractive asset for a future sale. That’s the buy-and-build playbook in action, and it's a cornerstone of modern private equity value creation.

Adapting Value Creation for Economic Headwinds

Private equity firms don't operate in a vacuum. When the economic forecast calls for storms—think high inflation, soaring interest rates, and general uncertainty—the standard value creation playbook has to change. The days of relying on cheap debt and ever-expanding market multiples are over, replaced by a new reality where resilience is everything.

In this kind of climate, the focus of private equity value creation makes a sharp pivot. It moves away from financial engineering and drills down on fundamental business health. Think of it like battening down the hatches on a ship before a hurricane. You’re not worried about a new coat of paint; you’re reinforcing the hull, securing the cargo, and making sure the engine runs flawlessly. For a portfolio company, that means a rock-solid balance sheet and operational excellence are the top priorities.

Protecting Margins and Managing Costs

Inflation is a two-pronged attack on profitability. The cost of everything from raw materials to labor goes up, while at the same time, customers are pushing back hard on any price increases. The best PE firms don’t just react; they get ahead of the problem with aggressive, proactive measures. This is where true operational expertise really makes a difference.

Strategic pricing becomes an essential tool for survival. Instead of just slapping a 10% increase on everything, firms dive deep into their data. They figure out precisely which products and customer segments can handle price adjustments without a drop in sales volume, which requires a sophisticated grasp of the value they provide.

At the same time, cost management kicks into high gear. The idea is to root out inefficiencies everywhere, whether that means renegotiating supplier contracts, optimizing supply chains, or bringing in automation to reduce reliance on manual labor. This isn't about thoughtless cost-cutting; it's a surgical approach to building a leaner, tougher operational core.

Shifting Value Creation into Due Diligence

One of the biggest changes we're seeing in this environment is that value creation is no longer a post-acquisition activity. It's being pulled forward and baked directly into the due diligence process itself. Instead of buying a company and then figuring out how to fix it, firms are building a detailed operational blueprint before the deal closes.

This approach de-risks the investment right from the start. Operating partners get involved much earlier in the process, identifying specific opportunities for improvement and validating their assumptions. It means that when the deal is done, there's already a clear 100-day plan on the table, ready to go.

This shift is more than just a feeling; it’s backed by data. In today's market, 46% of firms now stress embedding value creation during due diligence to get a better handle on their investments. At the same time, 38% point to revenue growth as their main focus, showing that top-line growth is still critical, even when times are tough.

This early-stage planning is a genuine game-changer. It allows firms to make an immediate impact and builds a foundation for success that isn't so dependent on having the wind at their backs.

The Rise of Technology and Turnarounds

In a more challenging economy, technology—especially artificial intelligence—is becoming a major differentiator. The latest numbers show that 45% of portfolios are now building AI opportunities into their value creation plans. They're using it to uncover efficiencies and insights that would be nearly impossible to spot with human analysis alone. To see exactly how firms are adapting, you can explore the latest value creation report from Alvarez & Marsal and get more details on their findings.

Tough times also create unique opportunities for complex turnarounds. PE firms with deep operational chops can acquire fundamentally sound businesses that are just struggling to navigate the macroeconomic headwinds, often at a great price. By stabilizing the company, fixing the operational issues, and getting it ready for growth when the cycle turns, they can generate incredible returns. It’s this adaptability and focus on operational grit that sets the top-tier firms apart, no matter what the market is doing.

How Financial Shifts Are Rewriting the PE Playbook

The days of cheap debt are over, and for private equity, that changes everything. For the better part of a decade, low interest rates made it easy to buy companies with borrowed money, but that era is officially in the rearview mirror. The recent spike in rates has completely upended the traditional formula for generating returns, making old strategies obsolete.

Think of it this way: debt has always been a powerful lever for magnifying returns. When borrowing was cheap, a PE firm could load up a company with leverage. Even small operational tweaks would lead to huge gains for investors because the cost of that lever was minimal. Now, that lever is incredibly heavy.

Financing costs have more than doubled, which means the bar for a successful investment is much, much higher. Every dollar of debt now takes a bigger bite out of a company's cash flow, directly eroding potential profits. Simply relying on financial wizardry or hoping the market will pay a higher price for the company later—known as multiple expansion—just isn't going to cut it anymore.

The New Math Demands Real Growth

This new environment forces a pivot. To get the same results, PE firms have to generate far more growth from the business itself, measured by EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). The math is stark, and it puts a laser focus on making deep, sustainable operational improvements instead of chasing quick financial wins.

Let's look at a simple example to see just how different the world is now.

To hit a 20% internal rate of return (IRR) on an investment held for seven years, a firm now facing a 7% interest rate has to drive annual earnings growth of about 4.2%. That's more than double the 1.7% growth that was needed when rates were at 3%. In essence, firms have to create almost twice as much real enterprise value to deliver the same returns to their investors. For a deeper dive into these market shifts, check out the latest deals outlook from PwC.

This isn't just a minor adjustment. It means that creating operational value has shifted from a "nice-to-have" to an absolute must for survival.

Longer Holds Mean No Time to Coast

Adding to the pressure, the market for selling companies has cooled off. With fewer buyers and tighter financing, PE firms are stuck holding onto their portfolio companies for longer. The quick three-to-five-year flip is becoming a rarity. This longer timeline demands a completely different approach.

Value creation can no longer be a short sprint. It's now a multi-year marathon. You can't just implement a 100-day plan and then sit back. Firms have to stay engaged, constantly looking for new ways to drive growth long after the easy wins are gone. This often involves:

- Rolling out second and third waves of operational improvements once the low-hanging fruit has been picked.

- Pursuing strategic bolt-on acquisitions a few years into the hold to spark new growth.

- Making long-term bets on new technology or international expansion that might not show a return for several years.

This reality gives a clear edge to firms with deep operational experience and a patient, long-term mindset. The pressure is on to build fundamentally better businesses—companies that are resilient and can grow steadily over time. It's a powerful reminder that real, lasting value is built through hard work, not just a clever financing structure.

Of course. Here is the rewritten section, crafted to sound like it was written by an experienced human expert.

Common Questions About Value Creation

As private equity has grown from a niche strategy to a major force in our economy, a lot of questions pop up about how it all really works. Let's break down some of the most common ones. My goal here is to cut through the jargon and give you a real-world understanding of how these strategies actually play out.

How Is Value Creation Different From Financial Engineering?

This is a great question, and the distinction is critical. The best way to think about it is like fixing up a house versus just refinancing the mortgage.

Financial engineering is the refinancing. It's about optimizing a company’s balance sheet, often by using debt to amplify returns without actually changing the business itself. It’s a numbers game, pure and simple.

Modern value creation, on the other hand, is the full-gut renovation. It's the hands-on, roll-up-your-sleeves work of making the company better from the inside out. We're talking about boosting sales, developing new products, making operations more efficient—building a fundamentally stronger, more profitable business. While a smart capital structure is still part of the toolkit, the real money today is made through tangible operational improvements, not just clever financing.

What Is the Role of a PE Firm's Operating Partners?

Think of operating partners as the master builders or expert general contractors of the private equity world. These aren't consultants with a slick PowerPoint deck; they are seasoned industry executives who have spent decades in the trenches, running businesses themselves. Their job is to work shoulder-to-shoulder with a portfolio company’s management team to make the value creation plan a reality.

They are the essential link between the firm's strategic vision and the company's day-to-day execution. This work gets incredibly tactical. An operating partner might be:

- Leading a complete overhaul of a company’s pricing model.

- Spearheading the implementation of a new ERP or CRM system.

- Professionalizing a founder-led sales team with structured processes and metrics.

- Guiding a complex project to untangle and optimize a global supply chain.

Essentially, they bring the specialized expertise needed to get the job done, ensuring the big ideas laid out in the boardroom actually translate into results on the factory floor or in the sales bullpen.

How Long Does a Value Creation Plan Usually Take?

A value creation plan is definitely a marathon, not a sprint. It’s designed to run for the entire 3-to-7-year holding period of an investment. It’s a continuous process that evolves over time, not a one-and-done fix.

The journey usually kicks off right after the deal closes with what’s called a "100-Day Plan." This is all about hitting the ground running, tackling the most urgent priorities, and scoring some quick wins to build momentum. After that, the PE firm and the management team map out a detailed, multi-year roadmap that guides the whole transformation.

A value creation plan is a living document. Initial cost-cutting might show results in the first couple of quarters, but major strategic moves—like a complex buy-and-build strategy or a big push into international markets—require sustained effort over several years to bear fruit.

It's all about constant improvement and execution. The end goal is to hand off a fundamentally better, stronger company at the time of exit, and that kind of deep-seated change takes both patience and persistence.

Are Value Creation Strategies the Same for Every Deal?

Absolutely not. In fact, a one-size-fits-all approach is a surefire way to fail in private equity. The best value creation plans are always highly customized. Before any deal is signed, a firm does a massive amount of due diligence to get under the hood of a company and diagnose its specific strengths, weaknesses, and, most importantly, its untapped potential. That deep analysis is the foundation for a truly bespoke strategy.

The specific levers a firm pulls will always be tailored to the company's unique situation. For example:

- For a high-growth SaaS company: The plan might be almost entirely focused on scaling the go-to-market engine, optimizing customer acquisition costs, and driving net revenue retention.

- For a mature industrial business: The playbook might center on lean manufacturing, supply chain optimization, and using technology for things like predictive maintenance.

- For a struggling business in a fragmented industry: The strategy could start with an intense operational turnaround, followed by an aggressive M&A plan to buy up smaller competitors and consolidate the market.

This tailored approach ensures that the firm’s expertise and capital are aimed precisely where they’ll make the biggest difference, maximizing the shot at creating real, lasting value.

Are you an emerging fund manager tired of wrestling with manual reporting in Excel? Fundpilot is your solution. We empower funds like yours to deliver institutional-grade LP reports, automate capital calls, and streamline compliance, all from a single platform. Stop drowning in administrative tasks and start focusing on what you do best—sourcing great deals and raising capital. See how Fundpilot can position your fund to compete with the giants by scheduling your demo.